Originally posted to livewire – Link Here

The past twelve months have been an improving story for investors; July to October was a brutal ride down, with global equity markets trading down in unison by close to 10% due to concerns around higher interest rates and higher oil prices. However, markets have rallied higher since much touted recessions have not materialised, and the Central Bank rate tightening has finished. Paradoxically, we are in an environment where negative economic data puts upward pressure on equity markets, as it is seen to bring forward the first round of interest rate cuts. Despite what feels like a bruising twelve months for investors, the ASX 200 has enjoyed a pretty good year, up +7.8% or (or +12.1%, including dividends).

The solid gain in the ASX 200 over the past year masks a large dispersion in returns, with financials, tech and retail companies posting solid gains, while energy and mining stocks have trod water. At year-end, many institutional investors cast an eye over the market’s trash to find some treasure to drive portfolio returns in the coming year. Invariably, several bottom-performing stocks will confound market expectations and stage remarkable comebacks! Unlike in previous years, the Dogs from June 2023 have not had a good year, with only one stock outperforming the ASX 200.

In this piece, we will examine the “Dogs of the ASX” in FY 2024, sifting through the market’s trash and look for treasure. We will also see how the 2023 Dogs performed, rate Atlas’ picks from 12 months ago, and examine the top-performing Dogs since 2010.

THE THEORY BEHIND THE DOGS OF THE DOW

Michael O’Higgins popularised a systematic investment strategy of investing in underperforming companies named “Dogs of the Dow” in his 1991 book Beating the Dow. This approach seeks to invest in the same manner as deep value and contrarian investors. O’Higgins advocated buying the ten worst-performing stocks over the past 12 months from the Dow Jones Industrial Average (DJIA) at the beginning of the year but restricting the stocks selected to those still paying a dividend.

Restricting the investment universe to a large capitalisation index like the DJIA or ASX Top 100 improves the unloved company’s chance of recovery in the following year.

Larger companies are more likely to have the financial strength or understanding capital providers (such as existing shareholders and banks) that can provide additional capital to allow the company to recover from corporate missteps or unfriendly economic conditions. Conversely, smaller companies in the Dogs of the ASX 200 from 2023, such as Lake Resources and Core Lithium, have been removed from the ASX 200 and appear to be fighting for their corporate lives.

RETAIL INVESTORS HAVE AN ADVANTAGE.

One of the reasons this strategy persists is that institutional fund managers often report their portfolios’ contents to asset consultants as part of their annual reviews. This process incentivises fund managers to sell the “dogs” in their portfolio towards the end of the year as part of “window dressing” their portfolio before being evaluated. Institutional fund manager selling of underperformers is especially prevalent in December and June of every year.

For example, in early July 2023, fund managers would have seen some pretty stern questioning from asset consultants about why they would have contractor Downer EDI in their portfolio after restating previously reported profits after overstating profits. Indeed, in early 2024, the company sued their auditor for failing to detect accounting irregularities created by my company executives!

Retail investors can afford to take longer-term views on the investment merits of any company that may have hit a speed bump, as retail investors are not swayed by asset consultants questioning short-term underperformance. Additionally, many underperformers see tax-loss selling around the financial year’s end, further depressing share prices in June. Often, the share prices of these underperformers rebound in the new financial year when this tax loss selling finishes and investors repurchase their shares.

ZEROS TO HEROES

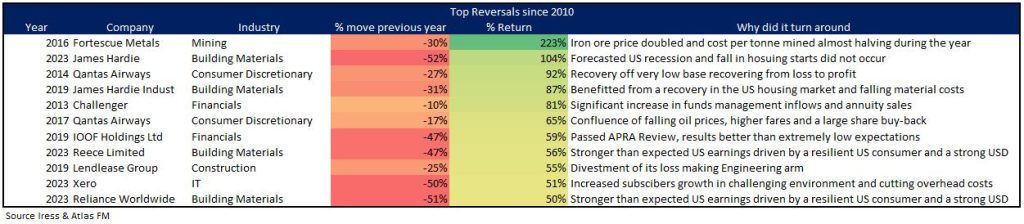

Over the past decade we have seen 11 companies stage share price returns turn around of greater than 50% over the twelve months after inclusion in the Dogs list for the prior year. Two companies, James Hardie and Qantas, have appeared twice. Miner Fortescue had the largest turnaround in 2016, adding over 200% after falling heavily in the prior year. 2015 saw company profits fall 88% on tumbling iron ore prices, and many in the market were concerned about the medium-term viability of Australia’s third iron ore miner, given debts of US$7.2 billion (despite no payments required until 2019). Sharply rebounding iron ore prices in 2016 saw a change in the miner’s fortune, with US$2.9 billion wiped from its debt pile and the company’s share price going from $1.74 to finish at $5.50.

Three common themes presented by the top reversal dogs have been:

1. Favourable moves in commodity prices – such as iron ore for Fortescue, building material costs for James Hardie, and low fuel costs for Qantas

2. Beating extremely low expectations – such as Challenger, Lendlease, Qantas and IOOF

3. Widely believed negative event does not occur – James Hardie, Reece and Reliance Worldwide all shined in 2023 when the expected US Recession and “Fixed Rate Cliff” in Australia did not occur.

DOGS OF THE ASX IN 2023

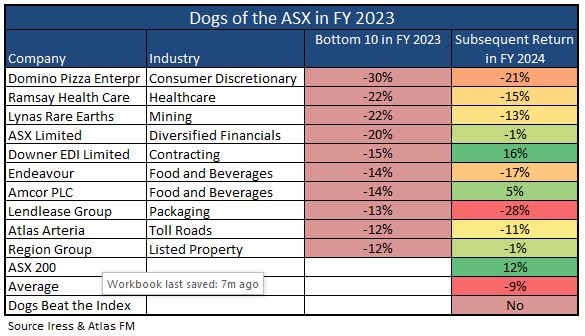

Over the past year, the Dogs from 2023 fell -9% and underperformed the ASX 200 and marks the largest underperformance of the Dogs Portfolio since 2015. What was also notable in 2024 was that the “Dogs” contained no significant outperformers. This contrasts with last July where the Dogs not only outperformed the ASX 200, but contained four stocks that finished the year 20% ahead of the index!

From the table above, only one out of the ten “dogs” of 2023 outperformed the index. Contractor Downer EDI shrugged off the earnings restatements of 2023 and saw its share price grind slowly upwards, highlighted by a positive result in February reporting operational improvements, higher margins and a 1 cent increase in the dividend.

Conversely, the pain continued in FY24 for Domino’s Pizza, Lend Lease and Endeavour. Dominos has continued to underperform in Asia due to lower Christmas period sales and earnings across Japan, Taiwan, Malaysia, and France while continuing to close stores across Europe. Endeavour has continued to underperform due to tighter regulations around its gaming machines, which are a high-margin segment of the hotel business. Lendlease has continued to underperform due to its high profile but unprofitable international construction operations, though in May the company announced the staged sale of the international business and a $500 million dollar buy-back.

OUR PICKS FROM JULY 2023??

When making our picks twelve months ago as to which of the Dogs from FY 2023 would rebound over the coming year, Atlas’ class mark would be a “C” with the teacher’s comment “must try harder next year”.

We expected that Atlas Arteria’s share price would rebound on improving operational performance and that 22% shareholder IFM would make a bid for the company. While over the past year IFM have increased their shareholding to 27% and the company has delivered record earnings, but threats from Marine Le Pen’s National Rally (RN) party to nationalise French banks, tollroads, airports and dismantle existing wind turbines has weighed on the stock. Similarly, Amcor, despite rallying in May on a strong third quarter result, has weakened in June and has finished the year with only a small gain.

Somewhat more successful was our pick that ASX would struggle in 2024. This pick looked very poor up until March 2024 with the ASX rallying alongside equity markets, however the Exchange’s share price took a tumble in June after revealing ballooning expense growth and increasing capital expenditure to replace its CHESS settlement system.

WHAT DOES THE CLASS OF 2024 LOOK LIKE?

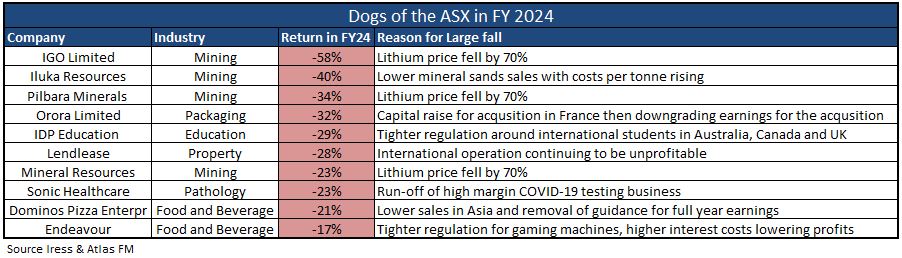

Looking through the list of 2024 underperformers, there are many new faces on the list, with Dominos, Lendlease and Endeavour the only companies to have previously been on the list of ASX 100 Dogs over the past ten years.

The key themes in the list of Dogs for the financial year 2024 are:

1. Fall in commodity Prices – IGO, Pilbara Minerals and Mineral Resources

2. Questionable International Expansion – Dominos Pizza, Lendlease and Orora

3. Tighter Regulation – Endeavour and IDP Education

4. Self-Inflicted Wounds – Sonic Healthcare and Iluka Resources

OUR PICKS FOR FY 2025

Every year, three or four companies in the Dogs of the ASX look like a poor addition to an investor’s portfolio on July 1st but will significantly outperform the market over the following year. In selecting a share price recovery candidate for the next year, we generally look at companies whose current woes are company-specific rather than caused by factors outside the control of their management team, such as commodity prices or government policies.

A rebound in the lithium price will see a significant recovery in the share prices of IGO, Pilbara Minerals and Mineral Resources, but Atlas does not possess a crystal ball that says with certainty that this will happen. Similarly, changes in government regulations for foreign students and gaming machines have weighed on the share prices of IDP Education and Endeavour, respectively. Government regulation on gaming machines does not appear to be abating, and on the 1st of July, the government increased international visa fees by 125%, making Australia the most expensive country to apply for a student visa.

Domino’s Pizza has had a rough few years, with its share price falling from $160 in late 2021 to $35 in July 2024, which indicates that a share price recovery could be on the cards. However, the company still looks expensive, trading on a PE ratio of 27 times and a recovery reliant on rebuilding a sprawling global business, particularly in France, Japan and Taiwan. Due to our lack of familiarity with the pizza markets in these countries, combined with the cost associated with closing stores, we are not picking the discount pizza maker to rebound in 2025.

Atlas’ picks for a recovery in the next 12 months are both Sonic Healthcare and Lend Lease. Sonic Healthcare had a weak 12 months due to higher inflation and currency headwinds, which culminated in a downgrade in May. However, profits in FY25 are expected to increase to A$1.7- 1.75 billion based on organic growth and recent acquisitions in the USA, Switzerland and Germany. Sonic trades at a discount on its share price in July 2019, however since then the company has increased earnings by 60% (or A$600 million), reduced debt and improved the quality of the business.

Lend Lease in FY25 looks similar to Downer EDI over the past year, an out of favour company with very low expectations. If the company executes on its exit plans from the international business and conducts the announced $500 million buy-back its share price will rebound. Exiting Lend Lease’s glamorous but unprofitable international business will be an addition via subtraction for shareholders.