Volatile Times

Unprecedented changes coming from the world’s largest economy driven by a President who can be described in the politest way as unorthodox and more realistically as grafting the world and, in particular, Americans on his quest for “Me the People”. Markets, economies, businesses and employees (i.e. Citizens) are trapped in a world being upended by acrobatics more amazing than Cirque de Soleil with dangerous, stunning and unbelievable moves with a fair share of backflips. Like all good circuses, no one knows what’s next, so we stay glued to the seat as spectators, oblivious to the real world outside and not willing to put a hand in the pocket, get down to work or invest in the future. The only certain thing is that the current instability will pass.

UNCERTAINTY makes everything harder

However, uncertainty creates opportunities that we see are beginning to surface. Here are some of my personal thoughts (not advice), which I am watching and interested in as the world changes. To quote one of the most famous Russians (topical at this point in time) – Vladimir Lenin — ‘There are decades where nothing happens, and there are weeks where decades happen.’ It feels like the latter. To steal another quote, this time from Howard Marks, “I don’t reach my conclusions with confidence or act without trepidation. There’s absolutely no place for certainty in the world of investing, and that’s particularly true at turning points and during upheavals. I’m never sure my answers are right, but if I can reason out what’s most logical, I feel I have to move in that direction.”

Let’s try and be reasonable.

Inflation seems likely to RISE not fall, which will impact interest rates and the liquidity interest rates provide or take away. Deglobalisation and rejigging the economic pipes can only increase the cost of goods and services (regardless of whether tariffs materialise or are just a deal-making headline).

A change we have seen globally is the politicisation of central bankers, unduly influenced by politicians who didn’t understand the GFC or the inflationary impact of expansionary fiscal policies. Those Central Bankers now understand that the short-term emergency measures they implemented, which lasted 15 years, have created asset bubbles, income inequality, and inflation. However, it took COVID and a fiscal splurge to match the monetary one to force the issue.

Inflation can be disastrous for society, and it is more likely central bankers will risk a fall in GDP and a tick-up in low unemployment rates to avoid inflation. This is one reason I believe interest rates, generally at historically normal levels, have more risk to the upside than downside and are perhaps being signalled by Jerome Powell and, to a lesser extent, Michelle Bullock. Those wishing for a return to 2-3% mortgage rates are likely to be disappointed.

So if inflation gets managed well as it appears to be, hats off to the Central Bankers for recognising inflation, resulting in rates higher for longer and bond markets signalling a need for fiscal responsibility from politicians, who have been stealing from tomorrow to give to voters today, we are likely to see liquidity drained out of the system.

In this process, one would expect to see asset allocation shifts and some decent returns.

Let’s try and be logical.

- Value may return vs Growth – Earnings today may be more important than forecasted TAM (Total Addressable Market) and revenue growth tomorrow. Ensuring that earnings exist, dividends are paid, gearing is suitable, and growth is in earnings, not the size of a potential market, almost sounds boring these days, but it shouldn’t.

- Credit spreads may/should widen from historic low levels. If liquidity is drying up, each dollar loaned needs more to attract it to being lent, and lower quality or higher risk funding needs to be rewarded.

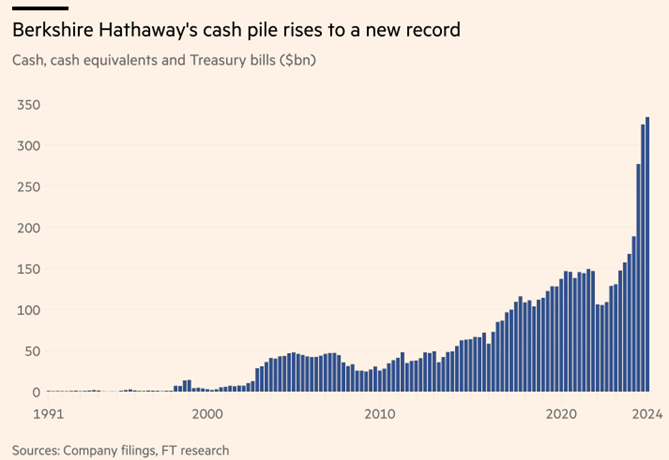

- Cash may return to being an asset that can provide income and opportunity (see last point) – The chart below shows the growth in Buffett’s cash pile, which suggests that he is excited by the possibilities and income it currently provides.

- AUD should rise – Australia, while struggling with productivity issues and possibly from having it too easy for too long, represents a strong investment destination for global investors. Our country is blessed with deep capital pools thanks to compulsory superannuation, a strong fiscal position (except maybe Victoria), a growing population, a large natural resource pool, the rule of law and enviable places to live. Improvements could be made by having a strong government cut red tape, developing the industry, and encouraging foreign investment. These changes could see the A$ back at parity with the US$ it was 10-15 years ago.

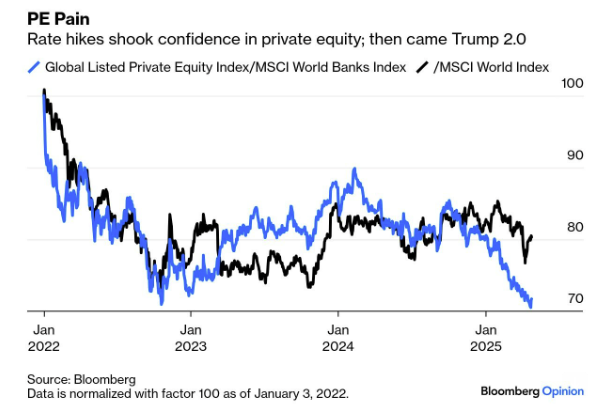

- Private Equity has been commoditised, being followed by Private Credit, on the back of abundant liquidity – it has been the poster child for asset bubbles – it is getting tougher with asset exits difficult and abundant dollars in PE funds at the ready, reluctant to chase businesses with optimistic PowerPoint presentations. The Red Flag is Private Equity buying and then selling to Private Equity – what extra value can one extract that the other can’t? Pass the Parcel minus the fees.

- Momentum cuts both ways – Markets have increasingly become driven by Momentum. The rise of passive over active (which increases the importance of indexing), machine learning, data scraping, trend following, meme following or sophisticated quant trading has created Momentum in a time of liquidity that feeds on itself. The liquidity hose created the desired Momentum during a crisis over 15 years ago and during Covid in 2020, with the short-term market “voting machine” dominating the style and direction of what has become long-term. Is it time now that the momentum reverses and it is time to step onto the market “weighing machine” scales? As quoted above, you cannot be certain, but I feel I must move in that direction. Momentum, like love, “cuts both ways” sorry Gloria

Gloria Estefan – Cuts Both Ways (iTunes Originals Version)

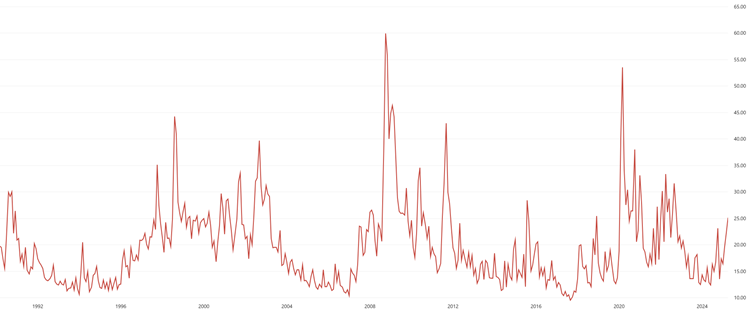

- Volatility will be higher going forward – deglobalisation, higher rates, and headline reactions should see volatility settle higher than the QE (Quantitative Easing) and ZIRP (Zero Interest Rate Policy) average of 2010-2022.

VIX measure since inception

In high-volatility environments, low-volatility returns increase in value.

Lower drawdowns, increased income, smoother returns – this is attractive in a time of heightened volatility. Don’t exit the market (see below), but look to limit drawdowns, have protection and stay nimble (have liquidity, transparency and ability to invest).

This brings the classic debate to the fore: Time in the market vs timing the market? Which seems now to be universally agreed to have been won by the former.

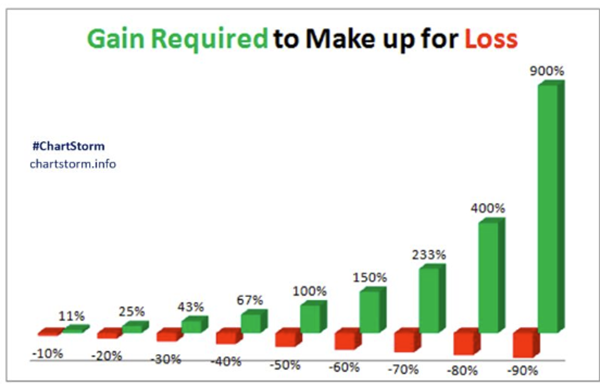

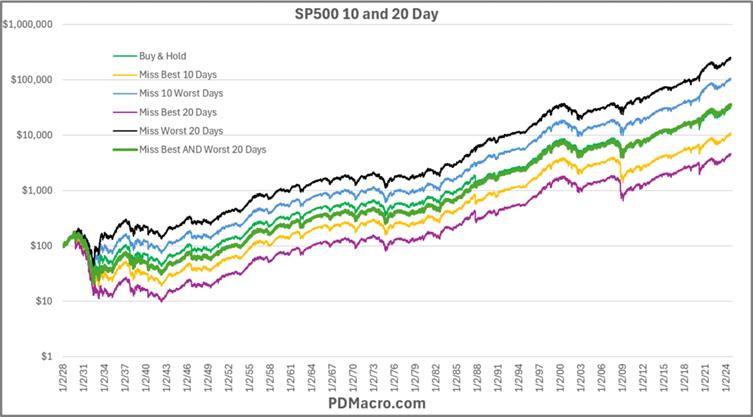

Below illustrates the cost and reward of being bad enough/good enough to “time the market” – I believe and agree that trying to time the market ends poorly over the long term….BUT….hear me out…

An old trading boss of mine at Lehman Brothers told me, “You can never beat VWAP (Volume Weighted Average Price)”, which, over the long term, I now agree with, but what was not said is that you don’t have to always be participating in the market or always buying the market. Buying on large drawdowns and selling on large market rips WHEN they happen can help, and this is where the Buy-Write strategy can effectively be put to use and where staying in the market and increasing investment on down days (staying nimble) and receiving income on up days, by selling away upside, can enhance your return and enhance your income generated. Note in the chart below that timing CAN be important if one is planning retirement, and somewhere on the right section of the chart below occurs to you – the importance of diversification and avoiding drawdowns.

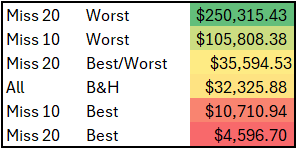

Furthermore, below are almost 100 years of returns on the S&P500. These are all logarithmic scaled charts, so they might not look wildly different, but if you look at the numbers, you can see that they really are. As discussed above, timing is not a viable long-term strategy, but having lower drawdowns accompanied by regular income/cash to buy on down days and generating income on up days by selling away upside can add to performance. My biggest takeaway from the chart and table below is missing the Worst and the Best days on the index result in a better return of being always invested. In some ways, this can reflect the return profile of an actively managed buy-write portfolio and can further be enhanced in Australia by utilising the franking on offer for taxpayers.

And here is the table of the chart above

Let’s wrap this up

So change is certain, and it feels like the magnitude of change now and going forward will be larger than it has been for some time – embrace the change that provides opportunities.

It is also a time to ascertain how returns are generated. In a time of volatility, that is, when asset prices fall (rarely does one panic when valuations jump aggressively), suddenly, there is a focus on risk-adjusted returns, not just the return – Why are risk-adjusted returns not ALWAYS the primary focus?

Have protection and stay nimble!