Aussie Firms Soul Patts and Brickworks’ $9 Billion Merger Send Their Shares Rocketing – CNBC

| Why ‘Boring’ Big Four Banks Remain Attractive Thursday, 22 May 2025 [If you received this from someone else and would like to subscribe, click here to receive our free weekly piece.] This article was originally posted on Firstlinks – Link Here The May 2025 bank reporting season was highly anticipated by investors, more so than usual. Many professional fund managers sold down their bank exposures in early 2024 due to concerns about recession, rising bad debts, and valuation concerns in the case of Commonwealth Bank. Selling the banks in 2024 proved to be a very painful trade for many fund managers, with the banks outperforming strongly last year. Indeed, the banks seemed poised for a big fall, with global economic uncertainty following President Donald Trump’s ‘Liberation Day’, which sent the ASX200 down 14% from its highs in February. However, the prophesied (and hoped for by those short the banks) doom and gloom for Australia’s banks did not eventuate this May, with all banks growing profits and again revealing minuscule bad debts. In this piece, we look at the major themes that played out over the May 2025 bank reporting season in the over 700 pages of financial results released, including the regional banks, awarding gold stars based on their performance over the last six months. Even for investors that don’t own the banks, looking closely at their results provides a window into the financial health of Australia. |

| Margin Pressure Net interest margins are always a major topic during the banks’ reporting season, with most investors going straight to the slide on margin movements in the immense Investor Discussion Packs. Banks earn a net interest margin (Interest Received – Interest Paid) divided by Average Invested Assets] by lending out funds at a higher rate than borrowing these funds from depositors or wholesale money markets. Whilst net interest margins came under pressure for the banks this half, most were able to offset lower margins with higher loan growth. For example, Westpac’s net interest margin decreased by 0.09% over the first half of 2025 to 1.88%. Although it is disappointing to have a lower margin, Westpac was able to grow its loan portfolio by $18 billion over the half, taking its loan book to $825 billion. Following the combination of a lower interest margin and higher loan portfolio, Westpac’s interest income was actually flat in the last half, despite the lower margin. Typically, Westpac and Commonwealth Bank enjoy a higher net interest margin than ANZ and NAB due to their higher weighting to mortgages, which enjoy a higher net interest margin than corporations that canvass banks in Japan or Europe for borrowing needs. In the first half of 2025, ANZ, Macquarie and Westpac saw small decreases in their net interest margins, with NAB able to hold steady across the half. All the banks mentioned higher competition for loans, though this was tough to detect in their financial results, with all banks doing a good job of growing their loan books to offset the margins. Bad Debts Remain Extremely Low Bad debts continued to remain low in 2025, with all the banks reporting extremely low loan losses. Bank of Queensland reported the lowest bad debts, 0.01% of gross loans, reflecting disciplined growth in their loan book, with all the big banks having less than 0.1% of gross debts as bad debts. The level of loan losses is important for investors as high loan losses reduce profits, and erodes a bank’s capital base. This reporting season has seen low bad debts translated into better-than-expected profits and, thus, higher dividends. Atlas sees that the low level of bad debts is a combination of the prudent management of risks in the loan book, low unemployment and more conservative lending than we saw from the banks 2000-07. However, it would be disingenuous to attribute current low bad debts entirely to prudent lending from the banks. APRA’s capital requirements announced in 2016 in response to the Basel III reforms to global banking effectively restrict banks from lending to developers that have not pre-sold 100% of their development and have a maximum loan-to-value (LVR) ratio on developments of around 65%. These requirements have seen developers switch to non-bank lenders and private credit funds that are not encumbered by these requirements. We believe the loans to developers, property syndicates, and troubled industrial companies that are impaired now sit with non-bank lenders and private debt funds rather than the big four banks. What we have seen in 2024 and 2025 are signs of stress in private credit funds, with various funds converting non-performing loans into private equity stakes and getting into residential property development as loans went south. While an APRA-regulated bank would have to declare this a bad debt, private credit funds have been slow to record these as losses. Not The Banks of 2007 Capital ratio is the minimum capital requirement that financial institutions in Australia must maintain to weather the potential loan losses. The bank regulator, the Australian Prudential Regulation Authority (APRA), has mandated that banks hold a minimum of 10.5% of capital against their loans, significantly higher than the 5% requirement pre-GFC. Requiring banks to hold high levels of capital is not done to protect bank investors but rather to avoid the spectre of taxpayers having to bail out banks. In 2008, US taxpayers were forced to support Citigroup, Goldman Sachs and Bank of America, and British taxpayers dipped into their pockets to stop RBS, Northern Rock and Lloyds Bank from going under. The Australian banks were better placed in 2008 and did not require explicit injections of government funds; the optics of bankers in three-thousand-dollar suits asking for taxpayer assistance are not good. The major Australian banks hold significantly more capital backing their loans in 2025 than pre-GFC or even ten years ago. Better-capitalised banks are safer investments for both investors and depositors. While the bank management teams congratulate their prudence in holding such high levels of capital, those with longer memories will recall the histrionic statements in 2015 when APRA forced the banks to raise $13.5 billion in extra capital. These capital raises were unusual as they were not made in response to a recession but rather to strengthen the banking system’s resilience against potential financial crises. In December 2024, APRA announced that additional tier 1 capital (bank hybrid notes) would be phased out of bank prudential frameworks. This will not be a large problem for the big banks, with all of them finishing the half with over 12% capital ratios. As many of these hybrids had franking credits attached to their coupon payments, the phasing out of hybrids sees franking credits build up on bank balance sheets. Buybacks Buying back shares on the market and then cancelling them is positive for both shareholders as it reduces the divisor on future bank profits, and bank management teams are awarded bonuses based on their return on equity (ROE). ROE increases as buying back shares reduces the equity divided by a bank’s return. Over the past few years, buy-backs have provided a consistent tailwind to bank share prices, with the banks themselves buying between 5-10% of the average daily volume on the ASX and then cancelling the shares. For example, since March 2022, Westpac has reduced its outstanding shares by 7%, buying back $7.5 billion in shares. Atlas has been reticent to swim against the tide of share buy-backs. Whilst no new buy-backs were announced during this bank reporting season, the banks still have large buy-backs to complete from previous years in addition to the neutralisation of the Dividend Reinvestment Plans (DRP) and, in the case of Macquarie Bank, neutralise the impact of shares issued by their Employee Share Plan. This should see $5.7 billion of bank shares bought back and cancelled in 2025 and will limit the impact of large market falls. Dividends In the May 2025 bank reporting season, the banks announced smaller increases in dividends than we have seen over the last few years, with the average dividend increase across the big banks being 1%. Of the big four banks, Commonwealth Bank had the largest dividend increase of 2.1%, with ANZ at the other end, holding the dividend the same as they did last year. These dividend increases were largely a byproduct of on-market share buy-backs that have been conducted over the last few years. For example, since November 2021, Westpac has reduced its share count by 7% after buying back $7.5 billion in shares, with other banks in similar stead. Regional Banks The regional banks walked away with two stars, being awarded to the Bank of Queensland, one for increasing dividends and one for low bad debts. In the past decade, the regionals have not seen many stars awarded. BOQ’s low bad debts are slightly below the other banks, and its dividend increase of 5.8% benefits from timing as it followed a 15% cut in the dividend in May 2024. Our Take In Australia, the big four banks dominate with a combined market share of 74%, following ANZ’s successful acquisition of Suncorp Bank. The closest to breaking into the market is Macquarie, with close to 6% of the market share. The two regional lenders, Bank of Queensland and Bendigo Bank, have a 3% market share each. As we have seen in the bank matrix at the top, regional banks face a competitive disadvantage compared to the major banks. They typically enjoy lower net interest margins and lower return on equity because they have a higher capital cost than the major banks. Here, wholesale funders require higher coupons on their bonds to offset their higher risks and greater geographic concentration. Additionally, the regional banks have limited access to the large pools of corporate transaction account balances that have historically paid minimal interest rates. |

Volatile Times

Unprecedented changes coming from the world’s largest economy driven by a President who can be described in the politest way as unorthodox and more realistically as grafting the world and, in particular, Americans on his quest for “Me the People”. Markets, economies, businesses and employees (i.e. Citizens) are trapped in a world being upended by acrobatics more amazing than Cirque de Soleil with dangerous, stunning and unbelievable moves with a fair share of backflips. Like all good circuses, no one knows what’s next, so we stay glued to the seat as spectators, oblivious to the real world outside and not willing to put a hand in the pocket, get down to work or invest in the future. The only certain thing is that the current instability will pass.

UNCERTAINTY makes everything harder

However, uncertainty creates opportunities that we see are beginning to surface. Here are some of my personal thoughts (not advice), which I am watching and interested in as the world changes. To quote one of the most famous Russians (topical at this point in time) – Vladimir Lenin — ‘There are decades where nothing happens, and there are weeks where decades happen.’ It feels like the latter. To steal another quote, this time from Howard Marks, “I don’t reach my conclusions with confidence or act without trepidation. There’s absolutely no place for certainty in the world of investing, and that’s particularly true at turning points and during upheavals. I’m never sure my answers are right, but if I can reason out what’s most logical, I feel I have to move in that direction.”

Let’s try and be reasonable.

Inflation seems likely to RISE not fall, which will impact interest rates and the liquidity interest rates provide or take away. Deglobalisation and rejigging the economic pipes can only increase the cost of goods and services (regardless of whether tariffs materialise or are just a deal-making headline).

A change we have seen globally is the politicisation of central bankers, unduly influenced by politicians who didn’t understand the GFC or the inflationary impact of expansionary fiscal policies. Those Central Bankers now understand that the short-term emergency measures they implemented, which lasted 15 years, have created asset bubbles, income inequality, and inflation. However, it took COVID and a fiscal splurge to match the monetary one to force the issue.

Inflation can be disastrous for society, and it is more likely central bankers will risk a fall in GDP and a tick-up in low unemployment rates to avoid inflation. This is one reason I believe interest rates, generally at historically normal levels, have more risk to the upside than downside and are perhaps being signalled by Jerome Powell and, to a lesser extent, Michelle Bullock. Those wishing for a return to 2-3% mortgage rates are likely to be disappointed.

So if inflation gets managed well as it appears to be, hats off to the Central Bankers for recognising inflation, resulting in rates higher for longer and bond markets signalling a need for fiscal responsibility from politicians, who have been stealing from tomorrow to give to voters today, we are likely to see liquidity drained out of the system.

In this process, one would expect to see asset allocation shifts and some decent returns.

Let’s try and be logical.

Gloria Estefan – Cuts Both Ways (iTunes Originals Version)

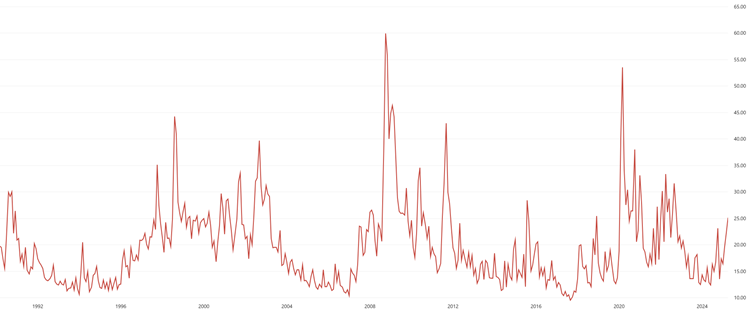

VIX measure since inception

In high-volatility environments, low-volatility returns increase in value.

Lower drawdowns, increased income, smoother returns – this is attractive in a time of heightened volatility. Don’t exit the market (see below), but look to limit drawdowns, have protection and stay nimble (have liquidity, transparency and ability to invest).

This brings the classic debate to the fore: Time in the market vs timing the market? Which seems now to be universally agreed to have been won by the former.

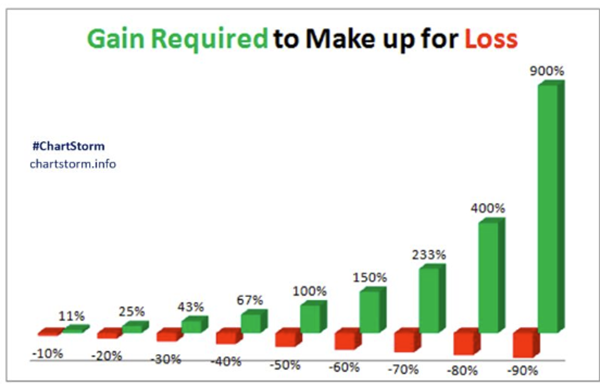

Below illustrates the cost and reward of being bad enough/good enough to “time the market” – I believe and agree that trying to time the market ends poorly over the long term….BUT….hear me out…

An old trading boss of mine at Lehman Brothers told me, “You can never beat VWAP (Volume Weighted Average Price)”, which, over the long term, I now agree with, but what was not said is that you don’t have to always be participating in the market or always buying the market. Buying on large drawdowns and selling on large market rips WHEN they happen can help, and this is where the Buy-Write strategy can effectively be put to use and where staying in the market and increasing investment on down days (staying nimble) and receiving income on up days, by selling away upside, can enhance your return and enhance your income generated. Note in the chart below that timing CAN be important if one is planning retirement, and somewhere on the right section of the chart below occurs to you – the importance of diversification and avoiding drawdowns.

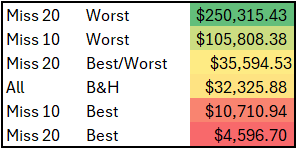

Furthermore, below are almost 100 years of returns on the S&P500. These are all logarithmic scaled charts, so they might not look wildly different, but if you look at the numbers, you can see that they really are. As discussed above, timing is not a viable long-term strategy, but having lower drawdowns accompanied by regular income/cash to buy on down days and generating income on up days by selling away upside can add to performance. My biggest takeaway from the chart and table below is missing the Worst and the Best days on the index result in a better return of being always invested. In some ways, this can reflect the return profile of an actively managed buy-write portfolio and can further be enhanced in Australia by utilising the franking on offer for taxpayers.

And here is the table of the chart above

Let’s wrap this up

So change is certain, and it feels like the magnitude of change now and going forward will be larger than it has been for some time – embrace the change that provides opportunities.

It is also a time to ascertain how returns are generated. In a time of volatility, that is, when asset prices fall (rarely does one panic when valuations jump aggressively), suddenly, there is a focus on risk-adjusted returns, not just the return – Why are risk-adjusted returns not ALWAYS the primary focus?

Have protection and stay nimble!