The Atlas High Income Property Fund had a solid month in November gaining +1.7%.

On Melbourne Cup Day the RBA met and decided to hold the cash rate at 0.75%, waiting to see whether previous rate cuts and $22 billion in tax refunds have boosted consumer spending and kept the unemployment rate in check. However, in his speech, the RBA Governor paved the way for further interest rate cuts in 2020.

The Fund remains populated with trusts with recurring earnings streams from rental income from long-dated leases to high-quality tenants. Due to leases that mostly provide for fixed price rental increases above the current of inflation, in the medium term, we expect steady growth in the distributions that the Fund is receiving from our investments.

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2020.

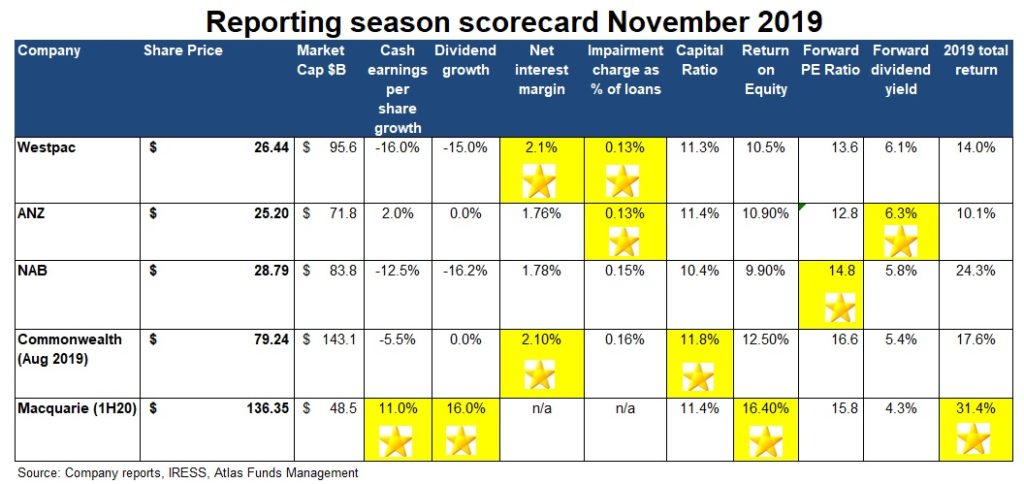

For much of the last decade the profit results for the banks were rather simple to analyse. Coming out of the GFC the major trading banks steadily grew profitability on the back of solid credit growth, declining bad debt charges and reduced competition as foreign competitors either exited the Australian market or were taken over. However, over the past two years, the profit results of the banks have been very complicated to analyse.

The Royal Commission on Financial Services has resulted in extensive remediation provisions, increased compliance costs and a spike in legal fees, at a time where credit growth has slowed dramatically and interest rates have moved towards zero. Additionally, Commonwealth, ANZ and Westpac all divested divisions, primarily in wealth and insurance, the areas of their businesses that were the source of the majority of their remediation charges.

In this week’s piece we are going to look at the themes in the approximately 800 pages of financial results released over the past ten days by the financial institutions that grease the wheels of the Australian capitalism and award gold stars based on performance over the past year.

Remediation

Customer remediation was a key theme for the results in 2019,

with banks compensating customers or taking provisions related to financial

advice, banking, insurance and consumer credit in response to the revelations

from 2018’s Royal Commission on Financial Services. Australia’s banks

have taken remediation provisions over the past 12 months of between $826M

(ANZ) and $1.1b (Westpac and CBA), with NAB around the $1.4b mark. ANZ’s lower

level of provisioning does not reflect any lack of prudence, but rather their

historically lower level of exposure to financial advice and funds

management. NAB’s higher level of remediation charges reflects their

desire to put MLC on solid footing before either selling or listing their

financial advice business in 2020.

No Stars given – remediation charges bad for

both customers and shareholders

Capital

While all banks have a core Tier 1 capital ratios above the Australian

Prudential Regulation Authority (APRA) ‘unquestionably strong’ benchmark of

10.5%, boosting capital was a feature the bank profit results in 2019. Westpac

increased their capital via both a $2.5 billion equity raising and cutting

their dividend, ANZ and CBA saw capital increase after selling wealth and

insurance divisions and not buying back shares to neutralise the earnings per

share impact and NAB’s final dividend was partially underwritten.

Normally increases in capital are only required when a bank is either

substantially increasing their loan book or are writing off the value of assets

in a recession, neither of which is the situation facing the banks in 2019 in

an environment of anaemic credit growth and low bad debts. These moves to

boost capital are in response to potential changes to capital requirements

across the Tasman discussed below and APRA’s moves to retain capital in the

Australian banking system.

Gold Star

New Zealand

New Zealand’s banking market is unusual in the developed world in that around

90% of lending is done by foreign banks namely the subsidiaries of Australia’s

major four banks and the country is a major capital importer. Most banking systems

have a similar structure to Australia, with domestically-owned banks dominating

lending and deposits. While this market dominance is often portrayed as a

takeover of the New Zealand banking system by sinister Australian institutions,

the concentration of market power is primarily due to the collapse of New

Zealand owned banks in the 1980s, with these banks being taken over and

recapitalised by Australian banks.

Late in 2018 the RBNZ released a consultation paper on bank capital

requirements, essentially saying that they would like the banks operating in

New Zealand to lift their Tier 1 Capital from 8.5% to a level of 16%, well

above APRA’s Australian standard of 10.5%. The impact of this decision (if

implemented) immediately would be for the Australian banks to inject around to

A$12 billion into their NZ-based subsidiaries.

The RBNZ consultation paper is based on the naïve assumption that the

Australian banks would do nothing in response to this additional capital

requirements, and that Australian shareholders would blithely fund New

Zealand’s aspirations to be the best-capitalised banking system in the world,

without any impact on pricing of mortgages in New Zealand or overall credit

availability in the shaky isles. In December 2019, the banks will gain clarity

as to how the RBNZ intends to implement their plans and in response, all of the

banks other than NAB are carrying high levels of capital.

In their results NAB took the most aggressive tone, suggesting that they will

reduce lending in New Zealand and reprice loans, an interesting move given that

in 2019 New Zealand was NAB’s most profitable market and the only division in

NAB that saw higher cash profits! If New Zealand’s capital requirements turn to

be less onerous than expected, investors may expect share buybacks from ANZ and

CBA.

Profit growth?

Across the banking sector profit growth reflected anaemic credit growth, falling interest rates and significant remediation charges, with earnings per share across the major banks declining by -8%. While some analysts and the banks themselves ignore these charges and talk about “normalised earnings”, we see this as specious logic. These remediation charges are not non-cash accounting charges, but actual cash outflows that impact shareholder dividends.

ANZ Bank grew cash profits per share by 2% courtesy of a very strong performance by their institutional bank and taking most of their remediation medicine in 2018. However, the gold star goes to Australia’s global investment bank Macquarie, which stands out with an 11% growth in earnings per share. Macquarie’s rising earnings per share is due to both successful expansions offshore and sidestepping most of the issues revealed by the Royal Commission.

Gold Star

Dividends

Given the level of remediation provisions and political scrutiny, no bank grew their dividend per share in 2019, though NAB and Westpac did cut their dividends to more sustainable levels. ANZ and CBA kept their dividends steady, with Macquarie sharply increasing their dividend ahead of profit growth, a luxury afforded to Macquarie by its low dividend payout ratio. Across the major banks, ANZ has the highest dividend yield at 6.3%, though this may be at risk in 2020 if the bank does not buy back stock to neutralise the impact of lost earnings from the sale of its insurance and wealth management divisions.

Gold Star

Bad debts

One of the biggest drivers of earnings growth over the last few years has been the ongoing decline in bad debts. Falling bad debts boost bank profitability, as loans are priced assuming that a certain percentage of borrowers will be unable to repay, and that the bank will incur a loss on the loan. Over the past few years, when analysts look through a bank’s financial statements one of the first pages that are turned to is the bad debt charge, as even a small rise may be interpreted as the start of a trend back to a normalised long-term level of bad debts around 0.3% of total loans. Bad debts remained low in 2019, with Westpac and ANZ reporting the lowest level of bad debts of a mere 0.13% of the loan book, aided by a stabilisation in the East Coast property market and improving affordability stemming from several interest rate cuts. On the business side there were no major corporate collapses over 2019.

Gold Star

Very Low-Interest Rates

Over the past 12 months the RBA has cut the cash rate from 1.5% to a historic low of 0.75% and the standard variable rate for an owner-occupier mortgage has fallen from 4.7% to 4.1%. While lower rates are positive for borrowers, low rates impact bank profitability and in particular their net interest margin. In 2019 the banks’ net interest margins [(Interest Received – Interest Paid) divided by Average Invested Assets] decreased across all banks. The fall was attributed to increased competition, customer remediation charges and the reduced funding benefit from the bank’s pools of deposits. For example, NAB has $88 billion in deposits that are currently earning interest rates close to zero, as lending rates fall and the bank (unlike the Swiss banks) cannot charge negative interest rates; the bank’s profit margin gets squeezed.

In his presentation to the market, NAB’s CEO made an interesting point that the RBA’s rate cuts were not achieving their goal of stimulating the Australian economy. He saw that borrowers were not reducing their monthly payments to spend on consumer goods and savers such as retirees who are likely to spend all of their interest income are getting a much lower rate on their term deposits. Thus, very low interest rates result in a wealth transfer between savers who would otherwise be spending their interest income to reducing the debts outstanding for borrowers, with a minimal positive impact on the economy.

Westpac and Commonwealth reported the highest net interest rate margin in 2019 which reflects both their greater focus on mortgages (which attract a higher margin than business loans) and the lower loan losses on mortgages compared with business loans.

Gold Stars

Our take

Investing in Australian banks is one of the major questions facing institutional and retail investors alike, with the banks comprising 25% of the ASX 200. We expect the banks to deliver around 3-5% earnings growth as they face low credit growth and increased regulatory scrutiny, though there are significant cost-out opportunities from rationalising their 1,000 branch networks around Australia, as the nature of changes from physical branch transactions to digital interactions between the banks and their customers that don’t require real estate and costly staff to execute.

However, if investors examine the wider Australian market the banks look relatively cheap, are well capitalised, and should have little difficulty in maintaining their high fully franked dividends. Additionally, their share prices are likely to see support over the next 12 months as the remediation and compliance charges stemming from the Royal Commission begin to abate. Commonwealth Bank and ANZ may conduct share buy-backs over the next year if the RBNZ adopts a more conciliatory strategy on December 5th when they release their controversial bank capital requirements.

The Atlas High Income Property Fund had a solid month in October gaining +1.2%. While global markets mostly posted a positive return, the ASX 200 declined, dragged down by the heavyweight banking and the mining sectors.

The key news over the month was the RBA cutting the cash rate by 0.25% to a new record low of 0.75%, we see that it is likely that there will be further cuts over the next year in response to higher unemployment. Currently, twelve-month deposit rates are at 1.6%, so to earn a mere $20 in interest per day a retiree needs to have over $500,000 on term deposit!

The Fund remains populated with trusts that offer investors recurring earnings streams from rental income rather than development profits. Due to fixed price rental increases, the distributions that the Fund is receiving from our investments are growing ahead of inflation.

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2020.

Since the United Kingdom voted in June 2016 to leave the European Union, concerns over Brexit have buffeted the share prices of Australian companies. As the result of the Brexit vote was announced, the ASX was one of the few world markets that was open and trading at the time when news of the vote came through. On that Friday over three years ago, A$42 billion was wiped off the market capitalisation of the ASX in a day that ruined the lunch of many fund managers and stockbrokers.

Most Australian investors would find the political machinations somewhat bewildering – both internally within the UK and in the UK’s attempts to thrash out a deal with Brussels. Both the prospects and the conditions contained in the Brexit deal are changing daily in the lead up to the Halloween 31st October deadline.

As we strongly believe that no expert has the answers as to what the Brexit political settlement will look like, in this week’s piece we are going to consider the impact in Australia of previous major world political shifts, and examine the actual profits earned by ASX 200 companies in the United Kingdom and the quantum that might actually be at risk.

While fear and uncertainty have dominated the animal spirits of the market it is hard to make the case that Brexit will trigger another GFC for Australian equities, nor indeed that a recession in the United Kingdom will have a dramatic impact on the profits of Australian listed companies.

Previous major changes

While a hard Brexit will harm the UK economy, we don’t see that it necessarily represents a doomsday scenario. In our opinion the impact will likely be closer to that of Britain’s withdrawal from the European Exchange Rate Mechanism (ERM) in 1992, which fixed the GBP against the European Currency Unit (ECU), the precursor to the Euro. In September 1992 the GBP initially fell against the Deutsche Mark and USD along with the FTSE 100 index. Despite tough talk at the time there was ultimately little impact on UK’s trade with the EU. Additionally, big export-orientated companies such as Diageo, Rolls-Royce, British American Tobacco and Unilever saw solid profit and sales growth in 1993 from a falling GBP. The ASX200 gained 34% in the year following Britain’s withdrawal from the ERM, though this was driven by domestic banks recovering from a property collapse in 1991, rather than positive influences from Europe.

Australian Profits coming from the UK

In the 2019 financial year the 200 companies that comprise the ASX 200 delivered a net operating profit after tax of A$107 billion. Of this, A$3 billion or 2.8% was derived from companies with operations in the UK, or companies that export goods to the UK.

The below table looks at the top 20 companies in the ASX 200 exposed to the UK, ranked by their UK sourced profits. These companies may face a hit on the translation of the A$3 billion profit sourced from the UK if the GBP falls further in the back end of 2019. However, after weakening in 2016 and 2017 following the vote, the GBP is now trading at A$1.85 which is very close to the level at which it traded before the Brexit vote in June 2016.

In the final column of the table we have looked at the goods and services supplied to the UK by these companies and the potential impact that a hard Brexit could have on demand. We see that it is difficult to make the case that all of the profits that Australian companies earn in the UK, or even the majority of this profit, is actually at risk.

The withdrawal from the European Union and the potential for the UK to fall into a recession will likely have the greatest impact on ASX-listed companies providing financial services, construction and travel. Fund managers Pendal and Janus Henderson have already seen reduced flows into their UK and European equity funds. NAB spin-off CYBG should see lower loan growth and higher bad debt. Increased barriers to travel and a lower GBP will impact outbound travel from the UK, and thus Flight Centre’s profits.

For a range of ASX-listed companies with operations in the UK, the impact on profits of a UK withdrawal from the European Union is a little less clear. A recession in the UK will impact sales at Unibail-Rodamco-Westfield’s two malls, though the flagship £3.3 billion London mall is fully leased. As the premier mall in the country, the boost to incoming tourism from a lower GBP should offset declining domestic retail sales. Similarly, Brexit-based stimulus plans may well benefit Lend Lease’s urban renewal projects

Along similar lines, the impact of Brexit on share registry activity at Computershare and Link is likely to result in fewer IPOs and takeovers in the UK initially, but this may be offset by higher regulation that increases share registry activity.

Finally, in the case of Australian companies providing healthcare services such as Sonic Healthcare, Ramsay and CSL, the UK’s withdrawal from the European Union might not have a substantial impact. In September the UK’s Chancellor announced a potential post-Brexit stimulus package that will see tax cuts and increases in funding for schools, hospitals and the police. Additional healthcare spending is likely to benefit the providers of pathology, hospital beds, and biotherapies that treat autoimmune diseases.

What about the rest of the ASX?

Looking across the rest of the ASX200, there are a range of companies that should see few effects from political decisions made on the other side of the world. Aside from negative sentiment, a no-deal Brexit will have minimal impact on Commonwealth Bank’s or BHP’s profits.

Cutting off the nose to spite the face

While the European leaders have talked tough, warning that there will be “consequences for Britain’’, it will hardly be in Germany’s or Europe’s interests to erect significant trade barriers between Europe and the fifth-largest economy in the world. In 2018 the EU enjoyed a trade surplus (exports minus imports) of £64 billion with the UK: the bulk of which was with Germany (£32 billion – mainly cars, pharmaceutical products and machinery), placing the UK in second position just behind the United States and ahead of France. Indeed, total export volumes to the UK account for nearly three per cent of German GDP.

Our take

For all the negativity, doom and gloom in the press and the markets over the past few weeks, we consider that the actual impact on Australian profits and dividends paid to shareholders will be quite minimal.

In 2018 the UK was Australia’s 14th largest export market (gold, wine, beef, lead and lamb), just a touch below Vietnam whose political issues get very little coverage in the Australian press. While there are many cultural ties between Australia and the UK, the UK is not an important trading partner for Australia. When the UK joined the EEC in 1975, Australia had to find other markets for the agricultural goods that previously had been shipped to the UK under preferential Imperial trade agreements. These goods became subject to EEC tariffs and consequently were replaced in British supermarkets with European foodstuffs.

This article was originally published in the Australian Financial Review

In 2018-19, the ASX 200 delivered a net operating profit after tax of $107 billion. Of this, $3 billion, or 2.8 per cent, was derived from companies with operations in the UK, or companies that export to the UK.

They hadn’t, as Latitude confirmed on Wednesday morning that its plans for a $3.2 billion public listing have been shelved indefinitely. “Despite extensive engagement with prospective investors the board and shareholders have determined not to proceed with the offer,” Latitude chairman Mike Tilley said in a statement.