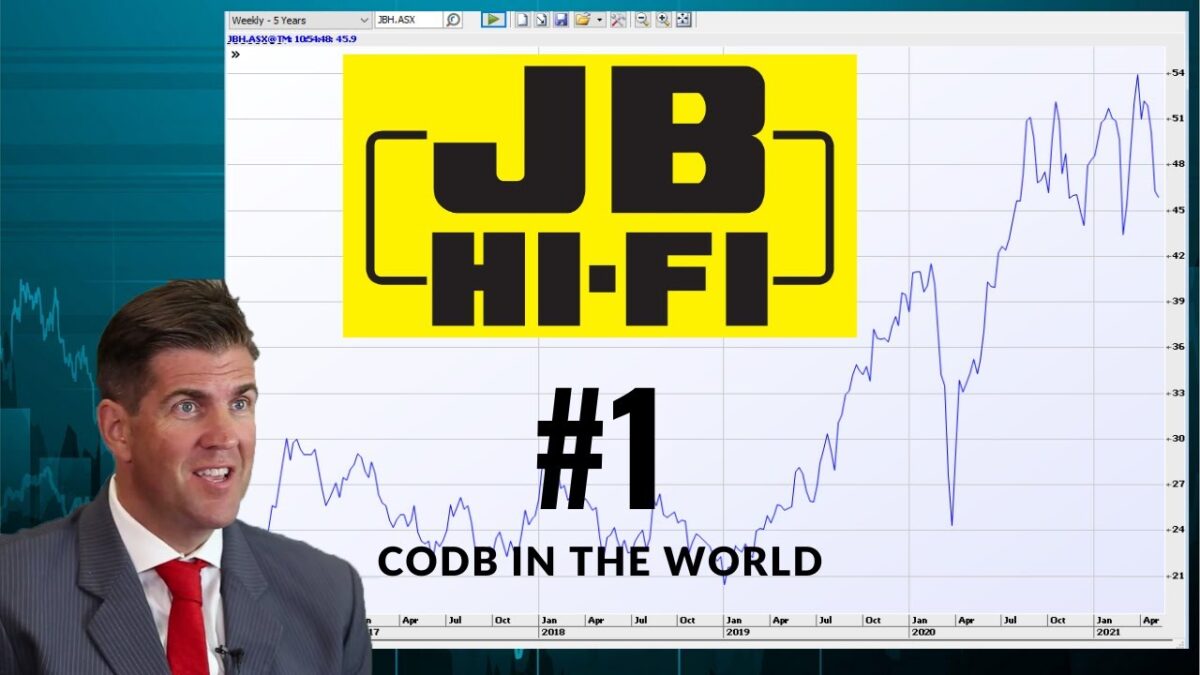

JB Hi-fi (JBH.ASX) has been one of the most polarising stocks in the market over the past few years and has consistently been one of the most heavily shorted…

JB Hi-fi (JBH.ASX) has been one of the most polarising stocks in the market over the past few years and has consistently been one of the most heavily shorted stocks on the ASX. In 2016 the consensus view was that JBH had overpaid for electronics and whitegoods retailer the Good Guys and had taken on too much debt, in 2017/18 the consensus view was that Amazon was going to permanently damage the company by undercutting pricing; and in 2020 rising unemployment would kill retail sales.

In all of these cases the nay-sayers have been proved wrong with JBH returning +150% over the past 5 years (vs ASX 200 +35%) and the stock being a graveyard for short-sellers Earlier this week JBH was again in the news releasing a very solid trading update for Q1 2021 (Q1 2021 sales up 11.5%), but also announcing that their CEO had jumped ship to clothing retailer Premier Investments.

Hugh Dive from Atlas Funds Management walks us through the finances and quality metrics of JB Hi Fi to understand how they’re a world leader in the cost of doing business, despite the relatively high Australian wages on the global scale.

The Atlas High Income Property Fund had a steady month gaining +0.7% with share prices continuing to recover from the dark days of early 2020 where the market was questioning the value of most classes of real estate. Over the month, several Trusts in the Fund provided positive trading updates, showing that rent collections from tenants are now back to pre-pandemic levels. Twelve months ago, commercial landlords faced government legislation preventing the eviction of tenants not paying rent if deemed to be impacted by Covid-19.

Concerns about inflation in the medium term was a key theme over April. The Portfolio is hedged well against rising inflation with rents and toll revenues inflation-linked. Indeed, as a legacy of the GFC where many companies struggled to refinance debt, most Trusts in the Portfolio now have long term fixed-rate debt. Rising inflation is likely to see higher profits as revenues grow faster than interest payments

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2021.

Fat Prophets CEO Angus Geddes is also worried about rising inflation and interest rates. Some CEOs at the Macquarie conference said domestic price pressures were building. Warren Buffett last week said Berkshire Hathaway has seen spiking demand and higher inflation across its businesses. “Australia’s housing market could run hot for another year,” Geddes says.

An incredible turnaround

Hugh Dive, chief investment officer of Atlas Funds Management, says Australian bank stocks are the best way to play the housing boom. “Rising house prices will enable banks to write back more of their bad-debt provisions this financial year and next. That will drive bank earnings and dividends higher.”

Dive was bullish on bank stocks after they crashed in March 2020, believing expected loan losses would be more moderate than the market thought.

His preference remains Westpac, followed by ANZ, which also reported this week, and the Commonwealth Bank. “Share-price gains might be slower from here, but the outlook for the Australian banking sector is the best in years. We believe bank stocks will outperform.”

The turnaround in bank stocks is incredible. A year ago, the banks forecast savage falls in house prices and investors braced for surging bad debts and bank dividend cuts. Today the banks predict double-digit house-price growth, bank dividends are up and there is speculation of share buybacks in the sector later this year.

Dive also favours JB Hi-Fi, a retailer at the epicentre of the property and work-from-home booms.

After soaring last year, JB Hi-Fi shares have eased in recent months. CEO Richard Murray’s surprise resignation and buyer fatigue in retail stocks have weighed on JB Hi-Fi, even though it noted strong sales growth over the past nine months in its latest trading update.

“JB Hi-Fi’s Good Guys division is performing strongly due to higher demand for white goods,” Dive says. “The market previously had concerns about the Good Guys acquisition and is still underestimating that operation. JB Hi-Fi will continue to benefit from housing strength over the next few years.”

Global equity markets staged a recovery in March, though Australia lagged global markets due to falling bond yields and weakness in Chinese equities based on concerns about a stalling recovery in the Middle Kingdom. Domestically the negative impact of a lockdown in Queensland was offset by falls in the unemployment rate and rising house prices.

The Atlas High Income Property Fund had a solid month gaining +3.7%, continuing to recover from the dark days of March 2020, when sections of the media questioned whether we would ever return to offices, shopping centres and toll roads. While most of the listed property sector’s share prices remain below where they were trading in February 2020, the lowly geared rent-collecting trusts that populate the portfolio are in good financial shape, collecting rents and paying distributions.

The Fund declared a quarterly distribution of $0.032 per unit. The distribution will be paid to investors in early April.

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2021.

April 2020, many experts predicted that residential real estate was set for a significant correction over the coming year based on expectations of a deep recession and sharp increases in the unemployment rate. Westpac’s economists forecasted an 8% fall in GDP in the coming year, unemployment to reach 10%, and a 20% fall in house prices and, based on this, took a $2 billion provision for expected loan losses.

Instead of falling, house prices accelerated over the past year with the latest CoreLogic RP Data Daily Home Value Index for March 2021 showing a +5.7% increase in national house prices led by Sydney and Brisbane.

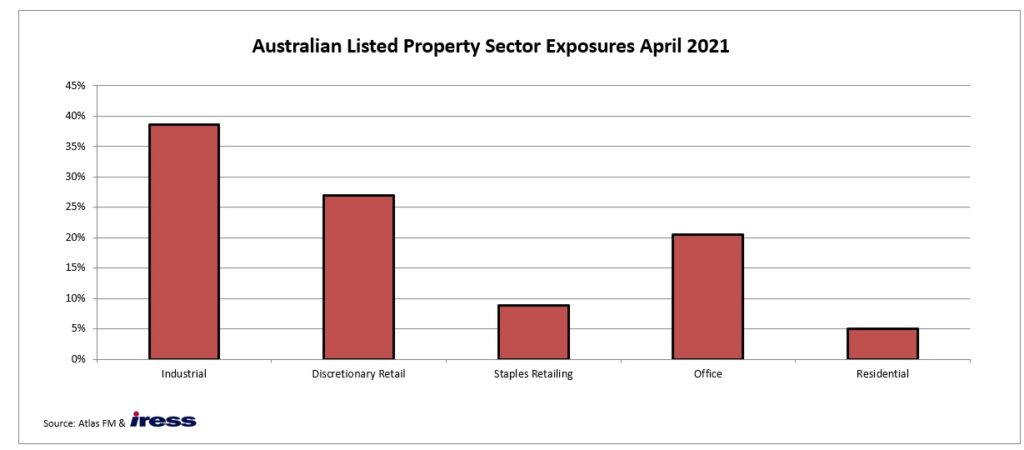

As the manager of a listed property fund, Atlas has recently received questions about gaining exposure to rising residential real estate prices without buying a house or apartment. However, as residential real estate is only a tiny portion of the overall listed property index on the ASX, this is an asset class that institutional investors largely ignore. In this week’s piece, we look at why listed property trusts avoid buying houses and apartments.

Listed real estate is not houses

Unlike the US or UK, where residential is a significant component of the listed property index (US residential REIT exposure 18%), the Australian index’s residential real estate exposure is relatively small at only 5% (see below table).

Further, the residual real estate exposure on the ASX consists of the development arms of diversified property trusts such as Stockland (mainly house and land packages) and Mirvac (predominantly apartments). Moreover, neither of these two trusts intends to hold residential property on their balance sheets over the medium term. Greater returns are available from developing and selling residential real estate rather than collecting rents. However, Mirvac has one build-to-rent project located in Sydney’s Olympic Park, assisted by some tax concessions, namely a 50% discount on land tax for the next 20 years.

Residential property has attracted little interest from institutional investors as retail investors have an investment edge. In the below chart, residential real estate comprised 5% of the S&P/ASX 200 A-REIT index in April 2021 or $6 billion. This is dwarfed by the value of the currently ‘beaten-up’ discretionary retail ($34 billion), industrial ($49 billion), and office ($26 billion) real estate assets listed on the ASX.

In our view, there are three structural reasons why retail investors rather than institutional investors are the primary buyers of residential real estate in Australia.

Capital gains tax breaks for homeowners ‘crowds out’ corporates

Firstly, in Australia, the tax-free status of capital gains for owner-occupiers selling their primary dwelling bids up the purchase prices of residential real estate. For example, when a company generates a $500,000 capital gain from selling an apartment, they would approximately be liable to pay $108,000 in capital gains tax. In contrast, the owner-occupier pays no tax on the capital gains made on a similar investment.

This discrepancy in the tax treatment allows the owner-occupier to pay more for the same home, anticipating tax-free capital gains not available to institutional investors such as property trusts.

Negative gearing

Similarly, individual retail investors benefit from the generous tax treatment in Australia that allows them to negatively gear properties. There are three types of gearing depending on the income earned from an investment property: positive, neutral and negative. A positively geared asset generates income above maintenance and interest costs, and obviously, neutral gearing generates no income after expenses and interest.

A property is negatively geared when the rental return is less than the interest repayments and outgoings, placing the investor in a position of losing income annually, generally an unattractive position. However, under Australian tax law, individual investors can offset the cost of owning the property (including the interest paid on a loan) against other assessable income. This incentivises individual high-taxpaying investors to buy a property at a price where cash flow is negative to maximise their near-term after-tax income and bet on capital gains.

Whilst companies and property trusts can also access taxation benefits from borrowing to buy real estate assets, a wealthy doctor on a top marginal tax rate of 47% has a stronger incentive to raise their paddle at an auction.

Yields on residential property too low

At current prices, the yield that residential property is not attractive for listed vehicles. At the moment, the ASX 200 A-REIT index offers an average yield of 4%. This compares favourably with the yields from investing in residential property. SQM Research reported that the implied gross rental yield for a 3-bedroom house in Sydney is only 2.7%, with a 2-bedroom apartment yielding slightly higher at 3.4% in April 2021. After borrowing costs, council rates, insurance, and maintenance capex, the net yield is estimated to average around 1%. This low yield on residential real estate contrasts sharply with the average yield after costs on commercial real estate currently above 4.5%. As listed property trusts traditionally attract investors that are focused on yield and many property trust CEO’s are remunerated based on growing distributions per unit; there is a strong incentive for Listed Property trusts to buy higher yielding commercial property and avoid lower yielding residential assets.

While housing comprises the most significant component of the overall stock of Australian real estate assets and talking about house prices is the one sport that unites all Australians, residential real estate holds little interest for institutional investors, especially for income-focused investors such as Atlas Funds Management.

Speculating on houses and apartments is one of the few areas of investment where retail investors have an advantage over well-resourced institutional investors.In the future institutional investors could play a greater role in owning residential real estate as they do in the UK and the USA. However, this would require either the extension of further tax concessions to corporates or alternatively removing these concessions such as negative gearing from households, two politically very unpalatable courses of action.