Few businesses have felt the government mandated shutdowns more than global travel agent Flight Centre (FLT) that has seen its share price fall by 73% in 202…

Few businesses have felt the government mandated shutdowns more than global travel agent Flight Centre (FLT) that has seen its share price fall by 73% in 2020.

Hugh Dive from Atlas Funds Management reviews the company through the Quality Filter Model after FLT raised $700m. The outcome is that there’s too much risk ahead for FLT, despite the company being very well run and holding strong competitive advantages.

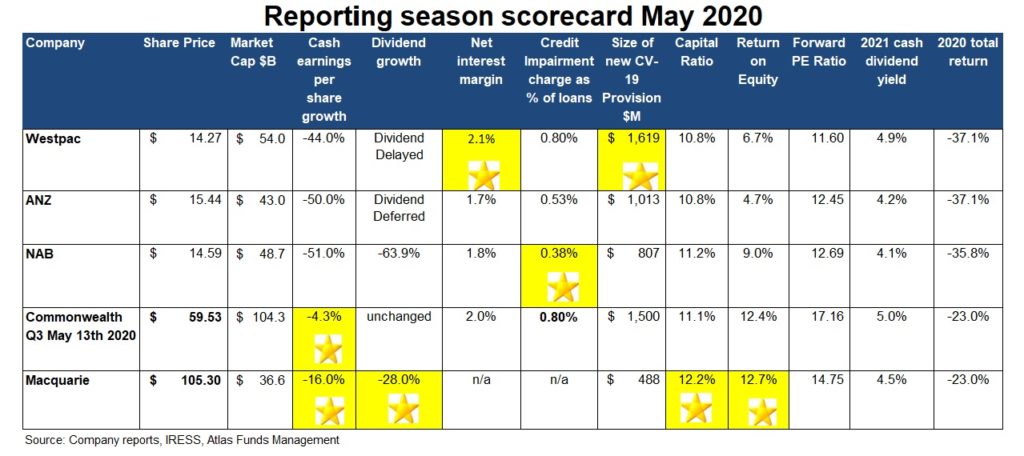

For much of the last decade, analysing the profit results for the banks was relatively straightforward. Coming out of the GFC the major trading banks steadily grew profitability on the back of solid credit growth, declining bad debt charges, and reduced competition as foreign competitors either exited the Australian market or was taken over. This changed with the Royal Commission on Financial Services in 2018, which had bank executive wringing their hands over remediation provisions and increased compliance costs during the profit results presented in 2018 and 2019. After CBA’s solid result in February 2020, this year was seen as the year when banking got back to normal; how wrong we were. I suspect that bank management teams would prefer being raked over the coals under the stern gaze of Commissioner Hayne, then in 2020 wondering whether a $1.5 billion provision for bad debts stemming from Covid-19 shutdowns will be enough?

In this piece, we are going to look at the themes in the approximately 800 pages of financial results released over the past two weeks, including Commonwealth Banks 3rd Quarter Update that came out on Wednesday morning. We will award gold stars based on performance over the past six months.

Uncertainty

Uncertainty was the key theme for the May results, with the banking sector making guesses as to the impact that rising unemployment might have on both house prices and more importantly, bad debts. Significant rises in business failures drive higher unemployment, which makes it difficult for stressed consumers to service mortgage and credit card debts. Previous downturns such as 1982/83, 1991 and 2009 were quite different from what we have seen in 2020. In the past unemployment rose gradually, allowing the banks some time to adjust their risk settings. The Covid-19 related shutdowns in the economy, by contrast, will likely see unemployment move from 5.2% in March to a number close to 8% when the ABS releases April’s unemployment rate on Thursday, with unemployment heading to over 10% by June. The reported unemployment rate is likely to be understated because of the JobKeeper Program. This dramatic step-change in economic activity would have been outside any of the banks’ stress tests.

Due to a timing issue, the banks reported profit results up until the 31st March. Therefore, these results capture at most two weeks’ worth of closures, omitting a significant period of impact. Similarly, the outlook statements issued over the past two weeks contain a degree of guesswork as to what the likely impairment changes will be over the coming year, a judgement that will determine the size of the Covid-19 provision for bad debts. NAB has taken the lowest provision, which would typically get it the gold star, but in the current environment, there are no prizes for being too optimistic. The market would prefer to see a provision written back rather than new provisions raised at the full-year results in October. Interestingly, the two banks with the biggest exposure to mortgages (CBA and Westpac) have taken the largest provisions, despite historically loan losses from mortgages being quite small. ANZ and NAB have greater exposure to business banking which tends to incur higher losses, but both have taken lower loan loss provisions.

Gold Star

Capital

All banks have Tier 1 capital ratios above the Australian Prudential Regulation Authority (APRA) “unquestionably strong” benchmark of 10.5%, despite the billions of dollars of provisions taken and, in the case of Westpac, a billion-dollar provision for an AUSTRAC fine. This allowed Australia’s banks to enter 2020 with a greater ability to withstand an external shock than was the case in 2006 going into the GFC. For example, in 2006 Westpac had a Tier 1 Capital Ratio of 6.8% as compared to 10.8% today, even after taking into account the $3 billion in provisions taken in May.

In the May results, there was plenty of self-congratulation from bank managements at their prudence for having such high levels of capital in 2020, allowing the banks to respond to Covid-19 from a position of strength. However, in our view, this is due to a combination of luck and pressure from the regulator: APRA (Australian Prudential Regulation Authority). APRA mandated in 2015 that the bank increase the capital held such that they would be “unquestionably strong and have capital ratios in the top quartile of internationally active banks”. This saw Australia’s banks raise $20 billion in capital, an approach that was unpopular at the time with both investors and bank management teams, and was considered excessively heavy-handed by APRA.

Furthermore, both ANZ and Commonwealth Bank sold their wealth management and insurance businesses between 2017 and 2020, which generated billions of excess capital. The capital was expected to have been returned to shareholders in 2019, but this was derailed by the fall-out from the Hayne Commission. NAB’s slow moves to sell MLC saw the bank raising $3.5 billion in late April at a price that was dilutive for existing shareholders. Macquarie comes out ahead of the trading banks, but this is due to the differences in the business model of the global investment bank that has seen lower loss provisions as well as an opportunistic capital raise conducted in mid-2019.

Gold Star

Dividends

Given the current level of uncertainty, the banks cut and suspended their dividends in May 2020 with encouragement from APRA. The latter announced that it expected “prudent reductions in dividends” during the crisis. Given the uncertainty facing bank boards as to the impact of Covid-19, ANZ and Westpac opted to defer their first half 2020 dividends and wait until August to determine whether a payment will be made. This caution reflects the timing of the decision in late April, with increases in bad debts yet to impact bank profits. Westpac and ANZ could have paid a dividend underwritten by an investment bank, but this would not have been in the long-term interests of shareholders. An underwritten dividend would have seen the investment bank selling newly issued shares on market throughout May to pay for the dividend, thereby diluting existing holdings and putting further pressure on the share price. NAB paid a 30c dividend in May, which was an exercise in financial gymnastics as it was coupled with a capital raising, which saw investors give NAB capital which was immediately returned. CBA’s dividend in February was unchanged, but we would expect a cut in August depending on the trajectory of bad debts. However, the sale by CBA of a 55% stake in Colonial for $1.7 billion is likely to allow the bank breathing room to pay a dividend in August. Macquarie cut their dividend but had a dividend payout ratio of 56%, which is well below their target range of between 60-80%.

Gold Star

Falling Net Interest Margins?

Last year the theme that was expected to dominate the bank results in 2020 was falling net interest margins. We are sure that compared to what bank management teams are actually facing in 2020, this now seems to be an issue of little significance. Banks earn a net interest margin [(Interest Received – Interest Paid) divided by Average Invested Assets] by lending out funds at a higher rate than that at which they can borrow these funds, either from depositors or on the wholesale money markets. The collapse in Australian interest rates in 2019 and increased competition for lending was expected to see the banks struggle to maintain net interest margins in 2020. The May 2020 reporting season saw net interest margins remain stable at between 1.7% and 2.1%, with the banks more heavily exposed to mortgages (CBA and Westpac) traditionally having higher margins than the business banks (NAB and ANZ). The Covid-19 crisis has seen many borrowers in particular corporations increase their loans to ensure that they had liquidity on hand, particularly in March 2020. ANZ, for example, saw a $29 billion increase in their corporate loan book commenting that a significant proportion of these new loans taken out were immediately put on deposit with the bank. Here we observe some management teams are using the playbook they used to combat the GFC crisis, where cash was king during a period where frozen financial markets halted bank lending. This does not appear to be the case in 2020, as we are facing a biological, in addition to a financial and social crisis.

Additionally, these new loans are being priced at higher rates than the existing loan book, which has supported the banks’ net interest margin. Going forward, we would expect loans to be repriced upwards when they come up for renewal, based on the banks’ pricing for higher levels of bad debts.

Gold Star – Australian banking oligopoly

Our Take

What to do with the Australian banks is one of the major questions facing both institutional and retail investors alike, as their share prices have fallen significantly in 2020 and they appear priced for the most pessimistic outcome. The remainder of 2020 will undoubtedly be tough for the Australian economy, but a big difference between the CV-19 crisis and previous crises has been the speed and size of the fiscal responses to CV-19. During the GFC, it took around 12 months for the politicians to respond to the unfolding crisis, mainly due to the impression that those most affected were bankers and US sub-prime borrowers.

In 2020 our political masters can see that the virus impacts voters. During the GFC peak stimulus spending in Australia accounted for around 1.8% of GDP, in 2020 the announced measures represent 9.5% of pre-crisis GDP. These measures will soften the impact on loan losses from the banks as stimulus payments flow into the economy. While the outlook for the banks looks uncertain, Australia’s banks have historically performed well coming out of crises that have reduced foreign competition and allowed them to absorb second-tier domestic banks. The threat posed by neo banks in 2019 may well recede as the CV-19 inspired “flight to quality” sees Neo bank deposits switch back to the major banks, at a time when losses on the neobank loan books are increasing.

April saw a recovery in the property market as new cases of COVID-19 (CV-19) slowed rapidly in Australia and the state governments, towards the end of the month announced some relaxations to the social distancing rules and the path to reopening the economy. Government programs such as the Code of Conduct for Commercial Tenancies have provided landlords with a mechanism for sharing the impact of falling sales by deferring rents, very different to the fear prevalent in March that rental income would go to zero.

The Atlas High Income Property Fund gained +13.1% reversing a proportion of March’s losses. Over the month, several holdings in the portfolio gave trading updates that indicated that their businesses were trading in-line with expectations given in February, with their tenants facing minimal impacts from CV-19 or in the case of supermarkets, chemists and liquor stores had seen increased turnover.

Unlike companies such as the banks, property trusts cannot retain earnings for a rainy day and have to distribute profits each year. The Fund has a strong focus on non-discretionary retail, and we expect that the June distributions from the underlying holdings will be ahead of meagre market expectations, especially as the economy emerges from the lock-down.

Human beings have consistently congregated in public places for shopping, dining and work since the Agora was built in Athens during the Fifth Century BC, it is hard to make the case that CV-19 permanently changes this pattern of human behaviour.

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2020.

Alongside the worldwide devastation as healthcare systems struggle to cope and deaths are well into the tens of thousands, the COVID-19 crisis is having a chilling impact on Australian corporates. Many companies are removing profit guidance given less than a month ago, cancelling dividends, raising debt, and in the last five days attempting to raise capital. Eleven years ago during the GFC many companies raised equity, often at deep discounts to their share price, as nervous bankers put pressure on management to shore up weakened balance sheets. In some situations, companies were forced to raise equity as their bankers were unable to refinance loans that had become due in a frozen credit market.

In this week’s piece, we are going to look at the various debt measures that we examine to assess a company’s solvency. These measures provide insight into whether management will be forced to raise equity during times of stress.

Gearing

Gearing is the most commonly discussed measure of a company’s debt. It indicates the degree to which a company’s business is supported by equity contributed by shareholders, as opposed to debt from banks and bondholders. Gearing is measured by dividing net debt by total equity (assets plus liabilities). During times of buoyant business conditions, companies with a high level of gearing generally deliver higher returns to investors. However, when the tide turns, highly geared companies have a riskier financial structure and have an increased chance of going into administration or having to raise equity to retire debt.

Most companies on the ASX have a gearing ratio between 25% and 35%. However, the level of gearing needs to be assessed in the context of the industry in which the company operates. Utilities such as Spark Infrastructure with regulated revenues can “safely” have a higher level of gearing than a highly cyclical stock such as Myer or Qantas. The latter two have more variable earnings and thus a variable ability to meet interest payments.

The key weakness in using gearing alone to measure a company’s solvency is that it assumes that the company’s assets can be realised for close to what they are valued on the balance sheet. The shortcomings of this approach are especially apparent for companies with a large proportion of intangible assets on their balance sheet, such as goodwill stemming from acquiring other businesses at prices above their net asset backing. In 2019 AMP’s gearing increased rapidly after the financial services company wrote down the asset value of its troubled wealth management and life divisions by $2.5 billion. Shortly after writing down the value of its assets, the highly geared AMP both cancelled its dividend and conducted a $650 million equity raising at a 16% discount to the share price at the time.

Companies such as Medibank Private, Janus Henderson and A2Milk are in the fortunate position in 2020 of having no net debt on their balance sheet. As a result, each has a negative gearing ratio and is facing no anxious discussions with their bankers. By contrast AMP, Pact and OohMedia (which raised $167 million last week) all have high levels of gearing.

Short-Term Solvency

Short-term solvency ratios, such as the current ratio, are used to judge the ability of a company to meet their short-term obligations. The current ratio divides a company’s current assets by their current liabilities (i.e. liabilities due within the next 12 months). Firms can get into financial difficulties despite long term profitability or an impressive asset base if they can’t cover their near-term obligations. A current ratio of less than one would indicate that a company is likely to have trouble remaining solvent over the next year, as it has less than a dollar of assets quickly convertible into cash for every dollar they owe. A weakness in using this measure to assess the solvency of a company is that the current ratio does not account for the composition of current assets which include items such as inventory. For example, winemaker Treasury Wine reports a robust current ratio. However, a large proportion of current assets are inventories of wine which may be challenging to convert into cash at the stated value during times of distress (panic buying of wine notwithstanding).

A further limitation of the current ratio in assessing a company’s financial position is that some companies such the ASX, Coles and Transurban which have minimal inventories or receivables on their balance sheet. This occurs as they collection payment immediately from their customers, but pay their creditors 30 or 60 days after being invoiced. These companies will tend to report current ratios of close to 1. Alone, this figure would indicate that these companies may be in distress. Indeed Coles has a current ratio below 1, which far from being alarming is due to the nature of the grocery business. Suppliers such as Kellogg’s and Coke are paid on terms between 60 and 120 days after they deliver their goods which creates a large current payables balance, while the receivables balance is small when customers pay for their cornflakes or Diet Coke via direct debit. This favourable mismatch between getting paid and paying their suppliers allows Coles and Woolworths to report an alarming current ratio that is effectively a loan from their suppliers to fund the grocers’ working capital.

Interest Cover

A debt measure that we look at more closely than gearing is interest cover, as this measures cash flow strength rather than asset backing. Interest cover is calculated by dividing a company’s EBIT (earnings before interest and taxes) by their interest cost. The higher the multiple, the better. If a company has a low-interest cover ratio, this may indicate that the business might struggle to pay the interest bill on its debt.

Before the GFC, I had invested in a company that had significant asset backing held in the form of land and timber. Using gearing as a debt measure alone, Gunns appeared to be in a robust financial position. However, interest cover told a different story. The combination of a rising AUD (which cut demand for its woodchips) and weak economic conditions resulted in Gunns having trouble servicing their debts despite their asset backing, and the company ended up in administration.

As interest rates have trended downwards over the past decade, it has become easier for companies to pay their declining interest bills, so in general, the interest cover ratio for corporate Australia has increased. Across the ASX companies such as JB Hi-Fi, Goodman Group, Wesfarmers and RIO Tinto all have an interest cover of greater than ten times. At the other end of the spectrum Nufarm, Viva Energy, Boral and Vocus all finished 2020 with interest cover ratios less than three times, which is likely to result in some worried discussions with their bankers. Nufarm has since sold its South American crop protection business with the proceeds going to pay down debt.

Tenor of Debt

A very harsh lesson learned on debt during the GFC was not on the absolute size of the debts owed by a company, but the time to maturity – known as the tenor of the debt. The management of many ASX-listed companies sought to reduce their interest costs by borrowing on the short-term market and refinancing these debts as they came due. While this created a mismatch between owning long-dated assets that were refinanced yearly, it was done under the assumption that credit markets would always be open to finance debt cheaply. This strategy worked well until global credit markets seized up in 2008 and a range of companies such as RAMS and Centro struggled to refinance debts as they came due.

When looking at a company’s solvency during times of market stress, one of the critical items to look at is the spread of a when a company’s debt is due. If the company’s debt is not due for many years, management teams may not be forced by their bankers into conducting dilutive capital raisings during a period of difficult economic times. In the ASX over the next year Seven West Media, Downer and Southern Cross Media all have significant levels of debt to refinance, which may prove challenging in the current environment.

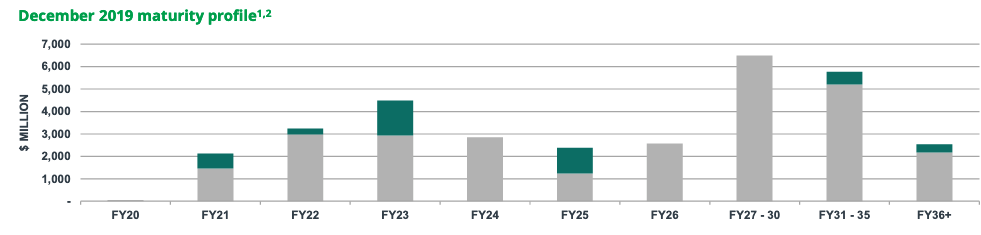

After the GFC many of the larger ASX-listed companies have sought to limit refinancing risks by issuing long-dated bonds in the USA and Europe. Toll road company Transurban does carry a large amount of debt, but as you can see from the table below, the maturities of these debts are spread over the twenty years with an average debt to maturity of 8.4 years.

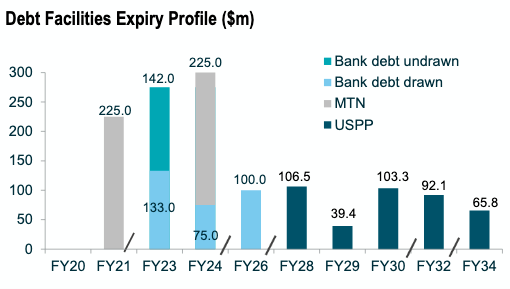

Similarly, at the smaller end of the market, the supermarket landlord SCA Property has minimal debt due over the next three years after issuing long-dated bonds in the USA. While COVID-19 is disrupting SCA Property’s business in March 2020, this spread of debt maturities positions this property trust better to ride out the current storm.

Covenants

Covenants refer to restrictions placed by lenders on a borrower’s activities and are contained in the terms and conditions in loan documents. These are either affirmative covenants that ask the borrower to do certain things such as pay interest and principal, or negative covenants requiring the borrower not to take on more debt above a certain level – for example; gearing must stay below 60% or an interest cover above three times. For investors, covenants can be difficult to monitor since, while companies reveal the maturity, currency and interest rate of their debts in the back of the annual report, disclosure on debt covenants is generally relatively weak.

Debt covenants were something that received little attention before the GFC when a covenant linked to Babcock & Brown’s market capitalisation triggered the collapse of the company. In June 2008, Babcock & Brown’s share price fell such that the company’s market capitalisation fell below $2.5 billion, and this triggered a covenant on the company’s debt that allowed its lenders to call in the loan. After this experience, very few borrowers will include a market capitalisation covenant in their debt, as this leaves the company vulnerable to an attack by short-sellers. More recently in 2019 when Blue Sky Alternatives breached covenants, bondholders called in the receivers to protect their loan.

In 2020 amid the COVID-19 crisis, debt covenants are once again in the minds of investors, particularly in the hard-hit media and listed property sector. In the media sector, a fall in TV advertising revenue of 10% is likely to trigger Seven West Media’s debt covenant of 4 times EV/EBITDA (enterprise value divided by earnings before interest, depreciation and tax).

In listed property, the embattled shopping centre trusts have more breathing room, as they entered 2020 with a lower level of debt. The key covenants for Scentre are gearing (less than 65%) and interest cover (higher than 1.5 times). For the gearing covenant to be breached, the independent valuation of Scentre’s assets would have to fall by 60% from December 2019; for the interest cover to be breached, earnings would have to fall by 60% assuming no change to Scentre’s cost of debt.

Hedging

In the context of debt, hedging refers to the addition of derivatives to limit the impact of movements in either interest rates or the currency in which the debt is denominated. Many Australian companies borrow in Euros, US dollars and yen – both to take advantage of the lower interest rates in these markets, but more importantly to borrow money for a longer-term. In 2020 the Australian dollar has fallen 12% against both the Euro and the US Dollar.

Companies that have significant un-hedged debt – such as building materials company Boral – will see their interest costs increase, especially if the company does not have enough foreign earnings to service their debt. This situation occurred in 2010 for Boral and required a dilutive $490 million to keep the company within their debt covenants. In December 2019 Boral’s debt was A$2.8 billion, but currency movements over the past 90 days have added $340 million to the struggling building materials company’s debt pile.

Our take

The upcoming year will be tough for Australia’s companies as the sudden step change in demand is very different to the falls in 1987,1991,2000 or 2008/09. While demand for goods and services fell during these previous times of stress, some companies are now facing a government-mandated shut-down of their businesses.

On a more positive note businesses are also likely to find more sympathetic bankers in 2020 than they faced in previous recessions, as well as massive government support. During the GFC, the banks themselves were not well placed to help businesses, as issues with the global banking sector were at the heart of the crisis. The banks were de-levering their own balance sheets, while struggling to explain collapsed credit markets and the problems created by complex financial instruments to hostile politicians. Given that the shutdowns from COVID-19 are a temporary state of affairs and in light of the massive fiscal stimulus, we would expect the banks to give many struggling firms a degree of leeway over the next year.

Australians have panicked and hoarded groceries. Coles has reported 20-30% grocery volumes above their peak Christmas periods. Hugh Dive from Atlas Funds Man…

Australians have panicked and hoarded groceries. Coles has reported 20-30% grocery volumes above their peak Christmas periods. Hugh Dive from Atlas Funds Management review the impacts to Coles’ profit and looks at whether it’s a buy in this current market.