In this weeks TT, Hugh Dive from Atlas Funds Management looks at the themes in the approximately 800 pages of financial results released over the past two we…

In this weeks TT, Hugh Dive from Atlas Funds Management looks at the themes in the approximately 800 pages of financial results released over the past two weeks including Commonwealth Banks 1st Quarter 2021 Update, awarding gold stars based on performance over the past six months.

In early 2020 it seemed that this year the banks were going to get their mojo back, rising profits were expected with the 2018 Royal Commission passing into the rear vision mirror along with falling compliance and remediation costs. After Commonwealth Bank reported their first-half 2020 earnings in early February delivering 11% profit growth that sent the bank’s share price surging over $90.

The only cloud on the horizon was the question as to how the banks were going to maintain profit margins with interest rates so low.

How wrong we were! In late March, a mere five weeks after reporting solid profit results, Commonwealth Bank’s share price had fallen 40% (like all banks) to $54. The financial press was wondering whether the several billion-dollar provisions each bank had taken for bad debts stemming from Covid-19 shutdowns will be enough?

October was a volatile month with most global markets falling between -3% and -7% in response to rising global cases of Covid-19 and uncertainty around the US election. Australian listed property also posted a negative return in October due to concerns about the lasting impact of the extended Melbourne lock-down.

The Atlas High Income Property Fund delivered a flat return in October. Over the month, we were pleased to see several trusts in the portfolio providing trading updates that revealed high rates of rent collection and that unpaid invoices from the period March to June were also now being received.

Additionally, in October, we saw several significant asset sales by large listed property trusts, mainly to foreign institutions, that were priced either at book value or at a premium to book value. As the share prices of the vendors currently trade at discounts between 20-30% to their net tangible assets, we see scope for the sector to be re-rated upwards, especially if some of these trusts trading at a discount receive takeover offers.

Go to Monthly Newsletters for a more detailed discussion of the listed property market and the fund’s strategy going into 2021.

Atlas are often asked by clients about the merits of investing in healthcare companies that offer cures, treatments or vaccinations that may both save lives and be very profitable for their investors. Biotechnology and pharmaceuticals[1] are probably among the most exciting and profitable sectors of the market in which to invest. In our view, however, they are also among the most challenging due to diversity of the industry and its complexity.

There are 50 healthcare stocks currently listed on the ASX offering a very wide range of products from medical devices, healthcare facilities to pharmaceuticals and biotherapies.

In this week’s piece we are going to look at investing in healthcare. We will outline the framework that Atlas uses to analyse healthcare companies that invariably have more potential pitfalls for investors than a standard industrial company.

Attractions of investing in healthcare stocks

Not only can healthcare investors gain a warm glow that they are helping humanity investing in companies that may cure life-threatening cancers or the scourge of Covid-19, but successfully developing drugs that respond to such illnesses can also be very profitable. Few investors gain a warm and fuzzy feeling from buying shares in Rio Tinto or Commonwealth Bank! Additionally, many companies in the healthcare sector are growing earnings far above the average of the ASX 200 with consistently high profit margins. Furthermore, companies that sell life-saving therapies to treat haemophilia (CSL) or produce implants that allow children to hear (Cochlear) are likely to see minimal impact on their revenue from macroeconomic concerns such as the US Presidential Election, Chinese bans on Australian exports, or indeed the overall health of the Australian economy.

Binary Outcomes and Extreme Specialisation

When investing in companies like Amcor or Transurban, an investor can make relatively accurate assessments as to the demand for packaging or trips taken on toll roads. By contrast, with healthcare few investors (even at the institutional level) would possess the scientific insight to assess the likelihood of success of different companies’ products in development.

With the biotech and pharma companies the investment case is frequently a binary outcome, namely either:

the science works and the product is approved for use in major healthcare markets such as the USA and the stock price goes up dramatically, or

b) it fails and the share price goes to zero unless the company can find new sources of funding or new products.

Earlier this week we were looking at Starpharma, a company that has some interesting products in testing designed to enhance the delivery of oncology drugs. In the unlikely event that the investor possessed a PhD in oncology and was able to assess the chance that Starpharma’s products will be approved, that unique investor’s scientific background would be of limited use in assessing the probability that CSL’s cardio-vascular biotherapy CSL112 will be successful in reducing secondary heart attacks. Indeed, the outcomes of many therapeutic development processes are unpredictable, even for specialised scientists working in the field.

Use a framework

When looking at a pharma or biotech company with plenty of promise, but lacking scientific expertise in their exact areas of research, Atlas would break down the analysis into manageable bites by asking the following eight questions:

What is the quality of management and have they had success before? Previous success in piloting drugs through the torturous and expensive FDA (United States Food and Drug Administration) and TGA (Australian Therapeutic Goods Administration) approval process provides some indication as to the probability of success.

Additionally, we will look at a company’s board for experience working in similar fields to the company’s exact field of expertise, as directors with scientific experience are more likely to be able to probe management. Often companies will have boards with limited direct pharma experience, but with a heavy weighting to directors with experience in finance and law. Directors with experience in these areas may be desirable in a large and well-developed company such as CSL, but less so in a small pharma company.

How close are the company’s drugs to approval? Looking at where a company’s treatments are up to in the US’s FDA approval process will indicate the level of investment risk. FDA approval is a requirement for sale in the most profitable healthcare market in the world and few companies would only seek Australian TGA approval which would limit sales to the small Australian market.

Companies with at least one product in end-stage trials are safer investments than those just beginning the investigative phases of development. On average it takes 12 years and over US$350 million to get a new drug from the laboratory onto the pharmacy shelf, with a 3% success rate for drugs to move from pre-clinical trials to full approval. We have seen many companies issue exciting prospectuses and raise capital based on the results of their treatment on mice, with minimal further developments many years later.

What does management own of the company? Here we are looking for substantial skin in the game from management. Ownership aligns the management team with investors, and incentivises them to push the product through the various phases of approval and perhaps towards a trade sale with a large pharma company.

How big is the addressable market? It is possible for investing in companies treating niche ailments to be profitable, for example Clinuvel does well with their treatments for rare genetic skin disorders. Ideally, however, when investing in healthcare stocks it is preferable to look at those companies operating in illnesses with large addressable global markets such as HIV/AIDS, cancer, heart disease, diabetes, neurological disorders and immunological diseases. Not only is the potential profit pool larger, but companies operating in these areas are more likely to attract a takeover bid from the big global pharma companies looking to restock their pipelines. In some situations, a large global company might make a takeover bid for a smaller company as a way of acquiring research and patents that is easier than going through the more uncertain process of conducting their own research. For example, in 2018 liver cancer therapy company Sirtex received a $1.9 billion bid for the company which was at a 78% premium to closing share price prior to the announcement of the bid.

Is there third-party endorsement? Third-party support adds to a company’s credibility and can be a positive indicator of future performance. The presence of large corporates or well-known fund managers on a company’s share register is one form of endorsement we look for, especially the multi-national fund managers with vast teams of analysts. An added benefit is that large investors are likely to have deep pockets to subscribe to new equity issues if the company requires additional capital. However, this factor should not be considered in isolation as well-respected managers have backed companies that have gone into administration. Furthermore, an individual healthcare company may in some cases be a very small and ignored portion of an institutional fund with assets in the tens of billions.

How is the financial strength and cash reserves? Whilst this point is germane to investing in all companies, the length and cost of the approval process for a drug are greater and more uncertain than for a new gold miner or retailer. If the company is required to make multiple dilutionary share issues just to stay in the game, its attractiveness as a potential investment declines. Similarly, if the approval process is slow and the capital markets unfriendly, the company may simply run out of cash prior to their therapies being approved, or may be unable to fund the next stage in the testing process.

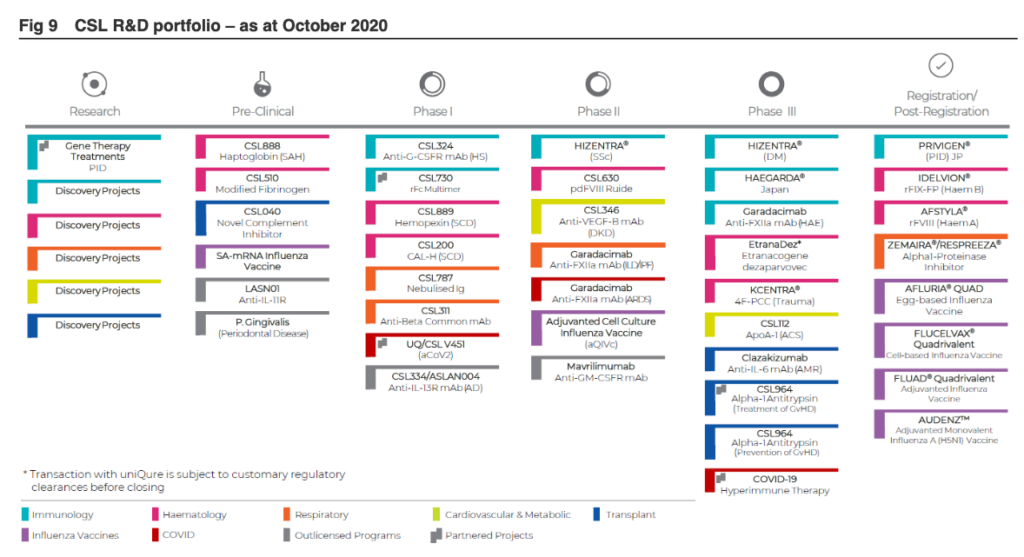

How diverse is the company’s pipeline? The number of investors that have made considerable gains in one tiny biotech is dramatically outweighed by those that have seen share prices plummet after a company’s only drug failed to win FDA approval. CSL shrugged off the failure of a competitor’s parallel trial of a plasma-derived product used to treat Alzheimer’s, as it had a range of other treatments both in the market and in clinical trials. The below table shows CSL’s pipeline.

8.How is the valuation? Valuation is the last measure that we look at when assessing whether to invest in a biotech or pharmaceutical company. As the vast majority of these companies are either losing money or are barely profitable, traditional valuation methodologies such as discounted cash flows, net asset value or dividend discount models generally require heroic long-range forecasts to derive a positive value. A company that passes a valuation filter is likely to be rejected as an investment if warning signals emerge when asking the preceding seven questions.

Our Take

Analysing a prospective biotech or pharmaceutical company for the first time can be daunting even for very experienced investors. The presentations are frequently full of unfamiliar medical jargon and optimistic accounts of how this particular drug or medical device will be a game-changer for those suffering a particular ailment. Conversely, when investing in banks like Westpac and Citigroup, the financial terminology and core services offered will be very similar, which allows the prospective investor to compare the two different companies easily. We consider that breaking the task down into manageable bites reduces the risk when investing in this potentially very financially rewarding sector allows the investor to compare the investment merits of heterogeneous healthcare companies.

[1] For our purposes the difference between biotech and pharmaceutical companies is that biotechs like CSL use technological innovations based on biological processes to address a health issue, whereas pharmaceutical companies develop therapeutics (medicines) specifically. For example, Pfizer is a pharmaceutical company that employs a chemical-based synthetic process to develop small-molecule drugs, while biotech covers a range of innovations from medical devices to using microorganisms or biologicals (such as blood plasma) to perform a process.

NAB and Westpac have already warned their results are unlikely to be pretty. On Friday, NAB said rising remediation charges, property impairments and an explosion in the scale of an underpayments problem at NAB would shave $450 million off the bank’s second-half result and cut 15 basis points off its Common Equity Tier 1 (CET1) ratio.

The last six weeks have seen some wild fluctuations in the share prices of many US tech stocks, which appear to have impacted the ASX’s tech sector. In August Apple (+22%), Facebook (+14%), Tesla (+74%), and ASX AfterPay (+33%) had strong months with share price gains significantly higher than the index. However, September has seen these high-flying companies come back to earth, falling between 10-20% over the past 15 days.

One reason why markets rise sharply is that when are more buyers than sellers. However, sometimes it is difficult (as it was in August) to determine a reason why individual stocks post strong gains, especially when a company has not provided new news.

Last month we saw the financial press clutch at straws trying to find the reason behind steep price movements that were markedly different from both the underlying index and the overall market. However, in the last week, it has been revealed that a large options trade from Japan’s Softbank, in combination with retail trader exuberance, seems to have prompted outsized gains in these prominent tech names. In this week’s piece, we are going to look at how relatively small trades in derivatives can have a large impact on underlying share prices.

Setting the Scene

2020 has seen a dramatic increase in the numbers of retail investors entering equity markets for the first time, typically opening brokerage accounts with the zero-cost platforms such as Robinhood in the USA and Commsec in Australia. Many of these new investors are stuck at home with stimulus payments, no sports to bet on, and uncertain economic prospects, so have gravitated towards investing in shares. Naturally, many of these often millennial investors have invested in tech stocks with which they are familiar. These stocks also have the appeal of delivering earnings growth in an uncertain environment. Therefore we have seen tech stocks globally gain sharply in 2020, trading on valuation measures that defy conventional logic. An example is the loss-making APT, trading on 44x revenue.

Institutional investors have also been forced to buy these growth companies. As these stocks become a larger part of the index they must be included in index funds. Active managers concerned about underperformance – and often ignoring valuations – buy them for fear of missing out.

Magnifying gains through options

Facing uncertain economic prospects and observing that the FAANG (Facebook, Apple, Amazon, Netflix and Google) stocks only seem to go upwards, an increasingly large number of investors have sought to magnify their gains by investing in call options rather than physical shares. Additionally, with companies such as Tesla sitting at a share price of US$2,200 (pre-stock split) and Amazon at US$3,100, buying call options for a fraction of the cost is seen as a cheaper way to participate in the rally.

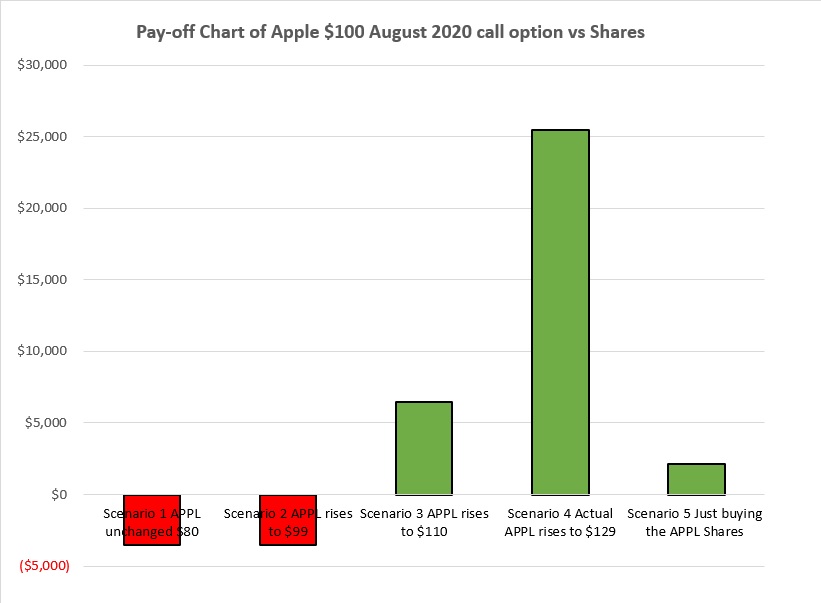

Call options are financial derivatives that give their holders the right to buy a specific asset by a particular time at a given price. For example, in early June Apple (AAPL) was trading at $80 per share; a three-month call option for/with August expiry with a $100 strike price was trading at $3.50 for one contract for 100 shares. So, for an initial outlay of only $3,500 – which buys 10 Apple call options – the investor has exposure to the movement for the next three months of $80,000 worth of Apple shares. If AAPL finishes August below $99, the investor loses the $3,500 premium paid in May; if, however, the price increases to $110, the investor makes a profit of $6,500 (after subtracting the price initially paid for the call premium).

As APPL finished August at $129 per share, the actual profit was much higher at $25,000, a significant gain for an initial outlay of $3,500.

From the above table, you can see that buying “out of the money” call options (options that have a settlement price far higher than the underlying stock’s current share price) in late May generated a substantially larger profit than the $2,144 that would have been gained from simply buying the AAPL shares at $80 and selling at $129 in late August. Though if AAPL had increased from $80 to $99, the holder of the $100 call option would have lost the $3,500 paid for option in early June.

Higher returns attract new entrants

Purchases of call options surged going into August in the USA. Small day traders spent around US$40 billion on call premiums according to data from the Options Clearing Corp. The options buying was concentrated in the popular tech sector names such as Apple, Facebook, Amazon, Netflix, Alphabet, and Microsoft. Most of these companies had a record amount of call options outstanding in August, and upward momentum in their underlying share prices generally.

Into this heated market, Japan’s Softbank reportedly paid $4 billion to buy short-dated out of the money call options with a notional value of $30 billion, with the counterparty’s major investment banks. This very large options position likely exacerbated the tech rally in August and then fuelled the fall in September as it was unwound.

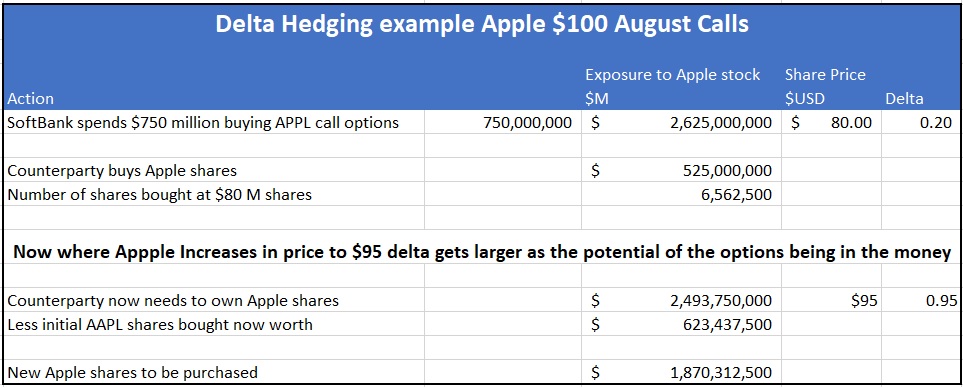

Delta Hedging

In an options trade, Softbank’s counterparty would buy a certain amount of stock to hedge their potential losses based on the sold call option’s delta. This is done to prevent significant losses in the event that the option finishes in the money and the counterparty has to deliver the stock to the option holder.

An option’s delta expresses the change in price a derivative is likely to see based on the price of the underlying company’s share price. The delta varies according to the distance between the current share price and the price at which the option can be exercised, as well as the time left in the option contract.

Take the above example of Apple $100 August call options. In late May with Apple’s share price trading at $80, the delta on these options was 0.2. SoftBank’s assumed purchase of AAPL options (along with the outstanding retail) for $750 million would have resulted in the counterparty selling Softbank the call options initially buying $525 million of AAPL stock to hedge their exposure.

However, as AAPL gained sharply through July and in particular in August, in our example SoftBank’s counterparty would have been forced to buy more AAPL stock in the market to delta hedge their exposure. As the delta of the options approached 0.95, in this example the counterparty bank would have needed to purchase around $1.8 billion in AAPL stock, putting upward pressure on the share price. On average the value of AAPL shares traded per day is around $1billion, and this increased to above $3 billion in August. It is likely that the “melt-up” of AAPLs share price was due to the forced buying of AAPL stock by investment banks looking to hedge their exposures to the derivatives contracts sold both the the NASDAQ Whale and the legions of retail investors.

Our take

Share price movements typically reflect the balance between the number of buyers versus sellers of stock on a particular day. However often the reasons behind price movements can be quite opaque. The August gains in tech stocks in the USA which probably had an influence on the ASX’s tech stocks such as AfterPay were likely influenced by the forced buying of tech names such as AAPL, due to the delta hedging activities of the investment banks that sold call options. Similarly, the falls in September are likely to be due to these positions being unwound. For example, Softbank almost certainly did not want to take delivery of $38 billion worth of AAPL stock in late August, preferring a cash settlement from the banks that sold them the options.

From these observations, one could take the view that buying out of the money call options is a sound investment strategy. However, around 80% of call options expire worthless with the seller collecting the premium. As a regular seller of call options in the Atlas High Income Property Fund, this has been our experience over many years. We find that buyers are generally too optimistic with regard to the expected near-term share price gains. Indeed, all of the options that we sold at the end of June, for expiry last Thursday on the 17th September, expired out of the money. This earned Atlas extra income that helps us pay our 7% yield.