In this note we will look at what is going on in listed property, the key themes to emerge over the past month from the profit results and how we expect listed property to perform over the next year. Given the name of our firm it would be remiss not to mention that this week marked the 60th anniversary of the publication of the Ayn Rand novel Atlas Shrugged. This novel provides an examination of whether the pursuit of profit is a noble enterprise or the root of all evil and the conflict in society between thinkers relying on facts and those defying reason, supporting their arguments on feelings.

Discretionary retail continues to face the challenges of on-line competition to bricks and mortar, a higher AUD, and slower inbound tourism which has reduced profit margins, particularly in clothing and footwear. Weaker retail sales limit the ability of shopping centre operators such as Scentre and Vicinity to raise rents and typically a rental contract will include a percentage of store sales. New clothing retailers Zara continue to take sales away from department stores like Myer, which is important given department stores are typically the largest rent payer in a shopping centre. Additionally, over the last year shopping centre landlords faced a few tenants closing stores due to insolvency such as Payless Shoes, Howards Storage and Pumpkin Patch.

Whilst the outlook for retail looks difficult, we do not see that shopping centres will become redundant, but they will need to evolve by favouring tenants that offer services that can’t be delivered on-line such as personal grooming and dining.

Office

In contrast to shopping centres, the Australian CBD office market looks pretty healthy for owners of office towers such as Dexus and Investa Office. Vacancy is the best measure of the health of the office sector, as empty floors in an office tower don’t earn rental income for the owners of office property trusts. Overall the market looks stable, but the picture across Australia is quite divergent with vacancy at a 23-year high in Perth being offset by very low vacancies in the Sydney and Melbourne markets. Sydney and Melbourne have benefited from the conversion of office towers into apartment buildings, which reduces supply, whilst Brisbane and Perth face excess supply from towers built towards the end of the mining boom.

Residential

Unsurprisingly the buoyant residential market in Sydney and Melbourne boosted the results of major residential developers Mirvac, Lend Lease and Stockland. Going into the profit results we were concerned that these developers could face defaults from buyers that have paid deposits for apartments (particularly in Melbourne). A buyer may refuse to complete a sale (thus forfeiting their deposit) if after completion the value of the property has declined or the buyer has had trouble obtaining finance. Our concerns were allayed in February with the developers reporting minimal defaults and healthy forward sales.

Industrial

Although the industrial assets continue to be priced higher, the underlying fundamentals have deteriorated with vacancies rising across the sector. Unlike office towers which are relatively homogeneous assets – which means, for example, that an accounting firm can take over space vacated by a financial planner – industrial sites are often configured for a particular tenant. A great example of this is the challenges the BWP face in filling sites vacated by key tenant Bunnings. The industrial trusts have continued to generate profits from re-zoning industrial property to residential. In October Goodman sold an industrial park in Sydney’s north west for $200 million to apartment developer Meriton Group.

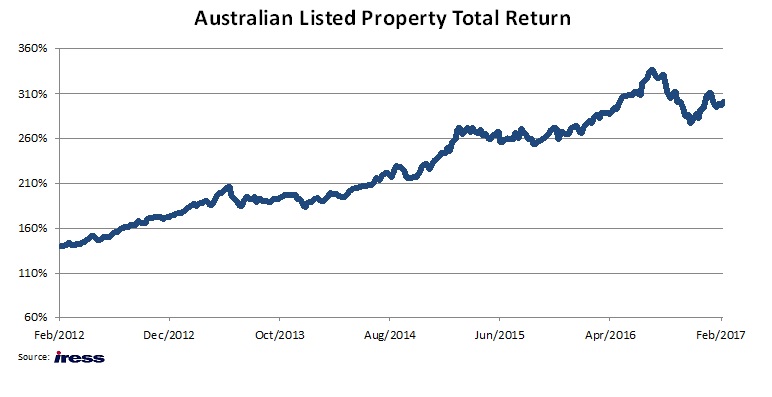

One Year Outlook

The total return (capital growth plus distributions) that investors can expect from Listed Property based on four financial components. These are; 1) distributions, 2) movement in asset values as measured by the capitalisation rate which is the rate of return on a real estate investment property based on the income that the property is expected to generate3) expansions or contractions in the market price to earnings ratio and 4) movement in the number of shares on issue (current buy backs or equity issues).

Over the next year, we see a small increase in the average distribution yield and a slight increase in asset values. However, due to concerns about interest rates it is hard to see an expansion in the market price earnings ratio above its current long term average and there are no significant buy backs currently in operation. Consequently, it is hard to make the case that the bulk of returns that investors can expect from listed property will not come from distributions.

Our Take

The Property Trust sector as a whole appears to be trading at a premium to fair value. We see that catalysts which propelled the sector up over the last three years have largely been played out and the majority of returns over the next 12 months will come from distributions and income from writing call options over existing holdings. The sector currently trades at a +26% premium to net tangible assets (14.2x forward PE and 5.2% yield). The portfolio strategy of the Atlas High Income Fund of populating the portfolio with higher quality domestic rent collectors combined with a derivative overlay strategy to enhance income should outperform in this market. Further, the focus on trusts that are delivering recurring yield should result in a higher distribution yield and lower earnings volatility for our investors.

Hugh Dive CFA

Chief Investment Officer

Insiders and insider trading

Insiders and insider trading